Call us

Call us

FOR EXISTING POLICY

FOR EXISTING POLICY

Have query on premium, payout or any servicing need?

Call us:

FOR NEW POLICY

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY (NRIs)

Note: Consent is provided to Tata AIA Life Insurance Company Limited to contact you by calling/giving missed call to the above numbers.

Thank you for sharing your details. To receive a call from Tata AIA Financial Advisor.

reCAPTCHA is not working.

No relevant search results found.

Health insurance provides financial support during medical emergencies, while life insurance ensures financial protection... Read more for your family in case of unforeseen events. Together, they form a comprehensive safety net. It covers various costs involved in the treatment incurred during a health emergency. It allows you to focus on timely treatment and recovery instead of arranging funds. It is also referred to as medical insurance plans. A suitable plan ensures access to hospital services, covering eligible expenses as per policy terms and conditions. Read Less

Health insurance is a contract where an insurer agrees to cover certain medical expenses in return for a regular premium payment. It helps reduce the financial burden of hospitalisation, surgeries, and other approved healthcare needs during illness or injury. Similarly, life insurance is a contract that provides a payout to the nominee in case of the policyholder’s demise during the policy term, helping secure the financial future of loved ones.

Health insurance plans in India may also include features such as cashless treatment through network hospitals, subject to policy rules. Choosing suitable coverage can support families in managing healthcare costs more steadily.

Award Winning

Tata AIA

Tata AIA Pro-Fit comprises of Tata AIA Health Pro, A Non-Participating, Unit-linked, Individual Health Insurance Plan (UIN: 110L180V01), Tata AIA Health Secure, A Non- Participating, Unit Linked, Individual Health rider (UIN: 110A050V01) & Tata AIA Health Buddy, Non-participating, Non-Linked Individual Health Product (UIN:110N183V01).Tata AIA Health Pro and Health Buddy are also available for sale individually.

An ideal health insurance plan caters to healthcare requirements specific to you and your family. Hence, you must choose the right type of health insurance policy for adequate coverage and exclusive benefits. Here are the common type:

Individual Health Insurance :Family Health Insurance:Senior Citizen Health Insurance :Critical Illness Insurance:Cancer Insurance:

Individual Health Insurance :Family Health Insurance:Senior Citizen Health Insurance :Critical Illness Insurance:Cancer Insurance:Health insurance covers hospital expenses during illness or injury. The insurer pays for medical bills up to the policy limit.

The specific procedures covered and the limits on these benefits can vary depending on your chosen health plan.

To encourage people to purchase a health insurance policy, the government offers tax4 deductions on premiums paid under Section 80D of the Income Tax Act, 1961 (old tax regime). These benefits apply to policies purchased for self, spouse, children, and parents. Accordingly, the premium paid towards your health insurance policy is eligible for tax deduction under Section 80D as per income tax act 1961 (under the old tax regime). The amount of tax deductions under your medical insurance plan is as follows:

Health Insurance Policy Purchased for |

Deduction Applicable to Self and Family |

Deduction Applicable to Parents |

Preventive Health Check-up |

Maximum Deduction Under Section 80D |

Self, Spouse, and Dependent Children |

₹25,000 |

- |

₹5,000 |

₹25,000 |

Self, Spouse, and Dependent Children + Parents |

₹25,000 |

₹25,000 |

₹5,000 |

₹50,000 |

Self, Spouse, and Dependent Children + Parents (Above 60 years) |

₹25,000 |

₹50,000 |

₹5,000 |

₹75,000 |

Self, Spouse, and Dependent Children (Above 60 years) + Parents (Above 60 years) |

₹50,000 |

₹50,000 |

₹5,000 |

₹1,00,000 |

Members of HUF (below 60 years) |

₹25,000 |

₹25,000 |

₹5,000 |

₹25,000 |

Members of HUF (a member is above 60 years) |

₹50,000 |

₹50,000 |

₹5,000 |

₹50,000 |

Therefore, you can claim deduction of up to ₹1,00,000 for the health insurance premiums paid under Section 80D in a financial year.

The following are covered in the health insurance plans in India.

The following are not covered in a health insurance plan

For Financial Security:For Changing Lifestyles:For Rising Medical Costs:For Tax Benefits:Offers Affordable Coverage:Covers Wide-Ranging Health Complications:

Eligibility depends on age, medical conditions, and insurer underwriting rules.

Criteria |

Specifications |

Entry Age for Adults |

18 years onwards |

Entry Age for Dependent Children |

90 days to 25 years |

Pre-medical Screening |

Required above the age of 45/55/60 years (depending on the plan) |

Age criteria

Adults can generally apply from 18 years onwards.

Dependant children may be covered from 90 days of age.

Maximum entry age varies across different insurers and plan structures.

Pre-medical screening

Medical tests may be required at certain ages, such as 45 or 55 years.

Senior citizen policies usually require screening before approval.

Screening helps insurers assess current health conditions more accurately.

Pre-existing diseases (PED) disclosure

Pre-existing diseases are covered after a waiting period, usually between 1 to 3 years. Insurers require disclosure of conditions such as diabetes, hypertension, kidney disease, or heart illness at purchase.

When choosing a health insurance plan, you should keep the following factors in mind:

Your policy coverage will determine what types of illnesses and surgeries you can claim. While choosing a health plan, pay attention to the benefits offered, such as hospitalisation expenses, daily cash benefit, COVID hospitalisation cover, critical illness cover, maternity cover, etc.

An important factor in choosing a medical insurance policy is the sum insured. Inflation should be considered when determining the sum assured. Family floater policies or senior citizen insurance will have better coverage if the sum insured is higher.

In India, there are different types of medical insurance policies. You can purchase individual health insurance, senior citizen health insurance, family floaters, or critical illness plans according to your needs. Additionally, you can enhance your coverage with Top Up and Super Top Up health insurance. It will be beneficial if your base sum insured gets exhausted during treatment. This option is available when purchasing and renewing your policy.

After the initial waiting period ends, your health insurance policy becomes active. Except for accidental hospitalisation claims, insurance companies reject claims filed during the initial waiting period. Further, the waiting period clause also covers pre-existing conditions such as thyroid, blood pressure, diabetes, etc. It also covers specific illnesses, treatments, and maternity cover. Make sure you choose a plan with a minimal waiting period.

A co-payment clause may be included in your medical insurance policy, which means a certain percentage of the claim amount should be borne by you (policyholder). The co-payment option does not affect the sum insured. While it may lower your premium to some extent, it increases your out-of-pocket costs. Hence, this clause should only be chosen if you can afford to pay off a portion of your hospital bills.

There are various sub-limits on health insurance plans, and the most common one is the room rent sub-limit. For example, if your medical insurance policy covers 3 lakhs with a rent sub-limit of 1%, then up to 3,000 per day your room rent will be covered. In case there is an increase in room rent, it will be your responsibility to pay it. Therefore, it is advisable to choose a health plan with no or minimal sublimit.

You should review the list of network hospitals where cashless claims can be submitted for an insurance company. A higher number of network hospitals in your area increases your chances of receiving cashless hospitalisation services.

Every year, medical insurance policies are renewed. In order to continue insurance coverage, policyholders must pay the renewal premium when the policy term is about to expire. When purchasing health insurance, it is beneficial to choose a plan that offers lifetime renewal options.

In health insurance plans for senior citizens, premium loading refers to the additional amount charged to risk-prone individuals. Choosing a medical insurance plan without loading will save you money. Claim loading is also charged by some insurers. This aspect usually increases your out-of-pocket expenses during the claims process.

An insurer's claim settlement ratio7 is an important criterion to assess their credentials. Always choose a company with a good claim settlement record. The ideal settlement ratio for a claim is above 80%.

Here are some key points to look into to ensure you pick the best health insurance plan that suits you and your family:

The first thing you need to check when browsing health insurance plans is the sum insured ranges offered and the medical treatments covered under the plan. The sum insured should be enough to cover most if not all, your medical expenses – including emergencies. Look for medical coverage that is relevant to your health status. For example, coverage for hospitalisation, ambulance charges, day care treatments, maternity treatments, AYUSH treatments, etc., are some common inclusions to look for.

Check the affordability of the health insurance plan. You may use online health insurance premium calculators, as they provide real-time and accurate estimates while allowing you to adjust the coverage options of your policy as per your requirements.

In addition, if you purchase it at a younger age, you can benefit from even lower premium rates. Furthermore, most online insurers will also offer discounts on their best health plans when you buy them online from their website and even have preferential rates. For example, Tata AIA offers preferential rates and discounts for women policyholders.

Your insurer is as important as your health insurance policy. Checking the insurance provider's reputation through reviews and testimonials can give you a good idea of their after-sales services.

Moreover, the insurer's Claim Settlement Ratio5 (CSR) provides insight into their efficiency in acknowledging and settling claims. Look for insurers with high CSRs and good customer reviews. For instance, Tata AIA's Individual Death Claim Settlement Ratio is 99.45% for FY 2025 - 26.

The best health insurance policies offer lifetime renewability. Check if your chosen plan offers this feature or if it has a maximum cut-off age for renewals. This is because you will most likely need a medical insurance plan when you are older.

Buying a new policy as a senior citizen can be expensive and difficult. Hence, check if your plan comes with this feature so you can continue with the same plan in your older years. Our Tata AIA Pro-Fit plan offers health coverage for a whole life, which means it is a lifetime plan offering coverage for up to 100 years. It avoids the hassle of yearly renewals.

Check if your health plan has pre-existing disease coverage and the corresponding waiting time to claim that coverage.

Check if the health insurance plan offers add-on riders5, as these can help extend your plan's coverage. Some common add-ons you should check for are critical illness cover, maternity cover, personal accident cover, OPD cover, accidental death cover, etc.

Check if the plan offers family floater options or variants, as these tend to be cost-effective if you want to insure your family members as well. They are also easier to maintain, as you will only need to pay health insurance premiums and track paperwork for one plan rather than multiple plans.

The eligibility criteria to buy health insurance differs depending on the type of health insurance plan. Traditional health insurance plans offer coverage for one policy year or up to three years and have to be renewed regularly after this period for continued coverage.

Mandatory pre-medical screenings are mostly only required for candidates over the age of 45 and for senior citizen health insurance plans before policy purchase.

Pre-existing illnesses almost always have a waiting period under health insurance plans and are only covered upon completion of the waiting period.

The waiting period can be at least 2 years and, however, depends on the type of disease and the insurer's specific policy terms and conditions.

For a more detailed list of documents for each claim type under Tata AIA, click here.

Here is how you can use a health insurance premium calculator to determine the premium for your health insurance coverage based on your requirements.

While younger applicants are charged lower health insurance premiums, older individuals tend to have higher premiums, considering the increased possibility of developing health-related issues or critical illnesses.

Health insurance premiums can also vary based on gender, with men paying more, considering factors such as their lower life expectancy rate compared to that of women.

If you have been suffering from pre-existing diseases or your family is prone to a critical illness, the health insurance premium will be higher to accommodate the increased risk.

Your lifestyle habits, such as smoking or the consumption of alcohol, can have a significant impact on the health insurance premium as there is a greater chance of contracting life-threatening diseases.

The type of plan you choose will also affect your health insurance premiums, as more coverage means higher premiums. You can determine the right option by using a health insurance premium calculator and comparing different health insurance quotes.

You can be eligible for this discount on your next policy year if you have not filed any claims in your previous policy year. The No Claim Discount or Bonus is applied during your policy renewals.

Health insurance policies allow you to claim compensation or insured medical treatments by filing claims. You can file two types of claims:

So, if you are wondering how to claim health insurance with Tata AIA, we have provided step-by-step instructions for both claims processes below:

If you are receiving treatment and paying at a hospital for an insured treatment or procedure, you file for a reimbursement claim through our website.

Ensure that you maintain all original bills and receipts, as you must submit them for reimbursement.

Here is how you can file for a reimbursement claim online:

Basis |

Health Insurance |

Mediclaim Insurance |

Coverage offered |

Provides comprehensive medical coverage, including hospitalisation, pre- and post-hospitalisation expenses, ambulance charges, and in some cases, compensation for loss of income due to an accident. |

Covers only hospitalisation treatment for injury due to accidents up to a pre-specified limit. |

Add-on covers |

Offers various add-on covers such as personal accident cover, critical illness cover, maternity cover, etc. |

Does not offer any add-on cover. |

Flexibility |

Provides flexibility to enhance or reduce coverage. Policyholders can also reduce premiums after a specified period by changing policy duration (e.g., long-term policies may offer premium discounts). |

Offers no flexibility in coverage. |

Critical illness cover |

Covers more than 30 critical illnesses (e.g., kidney failure, stroke, cancer), depending on the policy. |

Covers critical illnesses as per plan eligibility. |

Sum insured |

Ranges from ₹50,000 to ₹6 crore per year, depending on the plan. |

Usually does not exceed ₹5 lakh. |

Hospitalisation |

Not always required; day-care procedures can be claimed without 24-hour hospitalisation. |

Hospitalisation is mandatory to claim benefits. |

Premium |

Higher, as it offers extensive coverage. |

Lower, as coverage is limited. |

Lastly, let us clear a few presumptions you may have about health insurance policies. Despite growing awareness, health insurance penetration in India is low. Moreover, there are many health insurance myths. Some common misconceptions include:

Health cover applies to different types of medical expenses such as Surgical Cover, Daycare Cover, Hospital Cover, Disability Cover, OPD etc.

With Tata AIA health plans you can lock in your premium amount for a longer duration. Premium remains constant during the lock-in period unless the policy benefits or applicable taxes change.

The health cover benefits apply to worldwide treatment, providing the opportunity to avail of best-in-class treatment for your health issues.

Your lifestyle habits, such as smoking or the consumption of alcohol, can have a significant impact on the health insurance premium as there is a greater chance of contracting life-threatening diseases.

In addition to health coverage, you will also get life insurance coverage to secure your family in the event of your unexpected demise.

With our various fund options, you get the opportunity to invest for the long term and earn market-linked returns3 to build your health corpus.

You also have options to save funds with different types of discounts such as No Claim Rewards, Smart Lady benefits for female/girl child life assured, Digital Discount, Auto-Debit Discount, Super 30 Discount for life assured less than or equal to 30 years, Existing Customer Discount, etc., that can reduce your applicable premium.

Here are some of the most common health insurance terms:

Our experts are happy to help you!

Our experts are happy to help you!

There are several reasons why you should get health insurance, but the main reason would be to safeguard your finances from future medical emergencies and to ensure that you and your family stay covered.

The best health insurance plans are ones that will suit your needs and medical requirements. They are exclusive to your needs and specifications. But, if you are looking for health plans that offer comprehensive healthcare coverage, consider exploring Tata AIA Health Plans.

A family floater or family health insurance plan is ideal if you want comprehensive medical insurance for your family members — all under one plan.

Yes, you can claim a tax3 deduction on your annual health insurance premiums under Section 80D of the Income Tax Act 1961. You can claim additional deductions under Section 80DDB.

The Employees State Insurance (ESI) Act of 1948 offers health benefits to workers and their dependents in case of any unfortunate eventualities at work.

A health insurance plan is a legal contract between the insurer and the policyholder. The insurer promises to cover the insured individual's medical expenses in exchange for regular premium payments.

There are about 5 insurance companies that are registered under the IRDAI as health insurance providers. Apart from these companies, 26 other general insurance providers are registered under the IRDAI.

A minor cannot buy health insurance. However, their parents can include them in a family floater plan. As soon as they turn 18, they can buy their own health insurance.

Network hospitalisation refers to treatment provided at hospital with pre-established agreements with your insurance provider, usually offering cashless services. Here, the policyholder pays first and then seeks reimbursement from the insurer after treatment.

Insurers and types of claims determine how long it takes to settle a mediclaim. Cashless claims are generally processed within a day, while reimbursement claims may take few days.

There is no limit on how many claims can be made. As long as the claim falls within the sum insured and terms of the policy, multiple claims may be filed in a given year.

Yes. If you change jobs or leave your job, your employer-provided health insurance ends. A personal health insurance policy offers long-term financial security beyond group coverage offered by employers.

A medical check-up may not be mandatory. However, it is subject to the underwriting terms of the insurer and the policy. However, for younger individuals (below 45 years), a pre-policy medical check is often waived, unless they suffer from a pre-existing illness.

The 4 most purchased types of health insurance plans in India are individual health insurance, family health insurance, group health insurance and senior citizen health insurance.

Yes, you can buy more than one health insurance plan. For enhanced benefits, you can buy a traditional health insurance plan along with a fixed-benefit health plan such as our Tata AIA Life Insurance Pro-Fit.

Yes, you do not have to be an Indian citizen to buy health insurance. Foreign nationals and NRIs residing in India are eligible to buy health insurance, subject to the insurer's terms and conditions.

No, individuals already diagnosed with cancer cannot get insured under a new health plan unless it is a group health insurance policy under an employer. Therefore, you must purchase a health insurance policy that offers cancer or critical illness coverage.

During the policy term, the nominee can be changed. To update records, fill out a nomination form or write to the insurer.

Insurance companies will not cover expenses incurred after a policy lapses. To ensure uninterrupted coverage and claim settlement, renew within the grace period.

Smoking or chewing tobacco increases health risks and can raise insurance premiums. Insurance company takes lifestyle habits into account, and smokers or tobacco users may face higher premiums.

A cumulative bonus is the increase in insurance sum insured given by the insurer after every claim-free year. It acts as a reward for maintaining good health and not filing claims.

Health insurance can be cancelled for reasons like non-disclosure or fraud. Premium refunds depend on policy terms and whether claims have been made.

While there is no standard coverage amount for health insurance, there are two broadly accepted rules:

Today, a 5 lakh Mediclaim policy may only be enough to cover one person living in a Tier-3 city. This is because medical expenses can get extremely expensive in Tier 1 and 2 cities. Moreover, factors like medical inflation can also increase the treatment costs.

Generally, basic plans will only cover hospitalisation expenses and pre-existing diseases (after a waiting period). If you need critical illness insurance, consider looking for plans that offer 6add-on critical illness cover or built-in critical illness coverage.

Generally, only home isolations under the prescription of a doctor or certified healthcare professional through in-person or telemedicine consultations are covered by health insurance plans subject to the policy's terms and conditions.

The waiting period in health insurance is a time frame within which you will not receive coverage even if your policy tenure has been initiated. Most health insurance policies have a waiting period of 30 days, after which they will receive coverage.

In health insurance, a pre-existing disease (PED) is a health condition or illness you already would have been diagnosed with before buying the health insurance plan. These can be ailments like asthma, diabetes, high blood pressure, etc.

Generally, dental treatment is considered cosmetic procedures and are not covered under basic health insurance plans. Most insurers will only cover dental treatments or surgery if the damage to your teeth was the result of an accident or insured illness.

Yes, most diagnostic tests such as X-Rays, MRIs, and blood tests are covered under health insurance plans.

Insurance covers robotic surgeries only if they are advised by a surgeon. Insurance companies will not pay claims if a qualified surgeon does not recommend them.

Generally, health insurance covers pre-existing illnesses after a defined waiting period, which can range from several months to several years.

Generally, no. Insurers have a general/overall waiting period of 30 days before you can file any medical insurance claims. This waiting period is only waived in the case of accidents and other medical emergencies.

The first thing you can do is contact us, find out the reason for your claim refusal and file a complaint under our grievance redressal mechanism. If this does not work, you can always approach the IRDAI's Grievance Redressal Cell under their Consumer Affairs Department.

First, you must avail treatment from the hospital, pay your bills, and then contact us to initiate your claims process. Make sure you keep all the receipts/bills relating to your treatment.

A No Claim Bonus or No Claim Discount in health insurance is a percentage discount that is applied to your overall premium amount on renewal in the next policy year if you have not filed any claims in the previous policy year.

After your health insurance claim with Tata AIA has been filed and settled, your policy coverage (sum insured) will be reduced by your claim amount. As an example, if you have a health plan with a sum insured of 5 lakhs and file a claim for 3 lakhs, your health insurance coverage will be 2 lakhs after your insurer settles.

By paying the renewal premium before the due date, you can renew your mediclaim policy. Ensure timely renewal to avoid policy lapses.

If you meet the insurer's requirements and apply within the stipulated time frame, health insurance policies can be transferred without losing renewal benefits.

According to the insurer's guidelines, any increase in the sum insured is usually subject to a fresh waiting period.

Long-term policies or claim-free years may qualify for renewal discounts. Such discounts depend on the policy terms and conditions of the insurer.

The policy may lapse if not renewed before expiry. There is usually a grace period for renewal. Benefits may not continue after this period.

Yes, renewal allows you to modify or add riders6. According to the insurer's rules, the revised terms will apply.

Yes. A grace period of 15 to 30 days is usually offered by insurers for renewals.

Renewals are usually instant when done online. Upon receiving payment, the insurer will issue the renewed policy documents immediately, ensuring uninterrupted coverage.

Contact your insurer immediately if you miss the renewal date. Renewals are still possible during the grace period. After this, the policy lapses and fresh application may be required.

They’re not the same plan. The features and benefits of each plan are tailored to meet the needs of different individuals. The policy details should be reviewed before purchasing.

Yes, Tata AIA health insurance plans can be purchased online through the official website.

Pre-existing conditions are generally covered after a waiting period is completed. Depending on the specific plan selected, coverage details may vary.

The premiums are calculated according to factors such as age, sum insured, medical history, lifestyle, and added benefits.

Riders6 may include options like critical illness cover, accidental death cover, or hospital cash benefit. Riders6 are available depending on the plan and policy terms.

You can contact Tata AIA by their toll-free customer service number, official email id, or at a nearest branch office.

Tata AIA is a regulated insurer offering health insurance solutions under IRDAI regulation. Whether it suits you depends on your coverage needs, budget, and policy features.

Popular Searches

Last updated on dd MMM yyyy1782998491383

Disclaimer

The linked insurance product do not offer any liquidity during the first five years of the contract. The policy holder will not be able to surrender/withdraw the monies invested in linked insurance products completely or partially till the end of the fifth year.

Tata AIA Pro-Fit comprises of Tata AIA Health Pro, A Non-Participating, Unit-linked, Individual Health Insurance Plan (UIN: 110L180V01), Tata AIA Health Secure, A Non- Participating, Unit Linked, Individual Health rider (UIN: 110A050V01) & Tata AIA Health Buddy Non-Participating, Non-Linked Individual Health Product (UIN: 110N183V01) Tata AIA Smart Health Pro and Tata AIA Health Buddy are also available for sale individually.

Tata AIA Health Buddy Plan – Non-Participating, Non-Linked Individual Health Product (UIN: 110N183V01)

Tata AIA Health SIP (UIN:110L184V01) - Non-participating, Unit Linked, Individual Health Insurance Plan

Tata AIA Shubh Health Plus comprises of Tata AIA Health SIP - A Non-Participating, Unit-linked, Individual Health Insurance Plan (UIN: :110L184V01), Tata AIA Health Buddy, A Non-linked, Non-participating, Individual Health Product (UIN: 110N183V01 or any other later version). Tata AIA Health SIP and Tata AIA Health Buddy are also available individually for sale.

These products are also available for sale individually without the combination offered/ suggested. This benefit illustration is the arithmetic combination and chronological listing of combined benefits of individual products. The customer is advised to refer the detailed sales brochure of respective individual products mentioned herein before concluding sale.

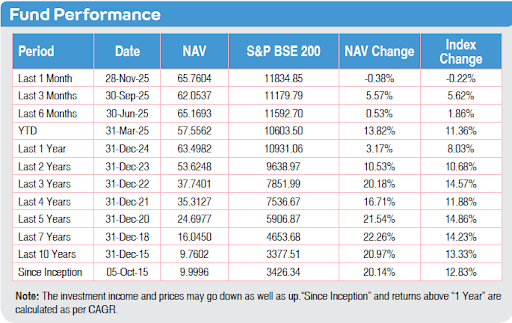

15-year computed NAV for Multi Cap Fund as of December 2025. Other funds are also available. Benchmark of this fund is S&P BSE 200.

2Get daily cash benefit of up to ₹20,000 on hospitalization & Up to ₹40,000 on ICU admission

3Market-linked returns are subject to market risks and terms & conditions of the product. The assumed rate of returns or illustrated amount may not be guaranteed and depends on market fluctuations.

4Income Tax benefits would be available as per the prevailing income tax laws, subject to fulfillment of conditions stipulated therein. Income Tax laws are subject to change from time to time. Tata AIA Life Insurance Company Ltd. does not assume responsibility on tax implication mentioned anywhere in this document. Please consult your own tax consultant to know the tax benefits available to you.

5Riders are not mandatory and are available for a nominal extra cost. For more details on benefits, premiums, and exclusions under the Rider, please contact Tata AIA Life's Insurance Advisor/Intermediary/ branch.

No Goods and Service Tax shall be applicable on Individual life insurance products as per prevailing laws. Tax laws are subject to amendments from time to time. If any imposition (tax or otherwise) is levied by any statutory or administrative body under the Policy, Tata AIA Life Insurance Company Limited reserves the right to claim the same from the Policyholder.

Tata AIA Life Insurance Company Limited is only the name of the Insurance Company & Tata AIA Health Pro & Tata AIA Health SIP is only the name of the Unit Linked health Insurance contract and does not in any way indicate the quality of the contract, its future prospects or returns.

The fund is managed by Tata AIA Life Insurance Company Ltd.

For more details on risk factors, terms and conditions please read Sales Brochure carefully before concluding a sale. The precise terms and condition of this plan are specified in the Policy Contract.

Past performance is not indicative of future performance. Returns are calculated on an absolute basis for a period of less than (or equal to) a year, with reinvestment of dividends (if any).

All investments made by the Company are subj ect to market risks. The Company does not guarantee any assured returns. The investment income and price may go down as well as up depending on several factors influencing the market.

Please make your own independent decision after consulting your financial or other professional advisor.

Unit Linked Insurance products are different from the traditional insurance products and are subject to the risk factors. Please know the associated risks and the applicable charges, from your Insurance Agent or Intermediary or Policy Document issued by the Insurance Company.

Various funds offered under this contract are the names of the funds and do not in any way indicate the quality of these plans, their future prospects and returns. The underlying Fund's NAV will be affected by interest rates and the performance of the underlying stocks.

The performance of the managed portfolios and funds is not guaranteed, and the value may increase or decrease in accordance with the future experience of the managed portfolios and funds.

Premium paid in the Unit Linked Insurance Policies are subject to investment risks associated with capital markets and the NAVs of the units may go up or down based on the performance of fund and factors influencing the capital market and the Insured is responsible for his/her decisions.

Please know the associated risks and the applicable charges, from your insurance agent or the Intermediary or policy document issued by the Insurance Company.

Insurance cover is available under the product.

The products are underwritten by Tata AIA Life Insurance Company Ltd.

The plans are not a guaranteed issuance plan, and it will be subject to Company’s underwriting and acceptance.

For more details on risk factors, terms and conditions please read sales brochure carefully before concluding a sale.

All Premiums are subject to applicable taxes, cesses & levies which will entirely be borne by the Policyholder and will always be paid by the Policyholder along with the payment of Premium. If any imposition (tax or otherwise) is levied by any statutory or administrative body under the Policy, Tata AIA Life Insurance Company Limited reserves the right to claim the same from the Policyholder. Alternatively, Tata AIA Life Insurance Company Limited has the right to deduct the amount from the benefits payable by Us under the Policy.

Auto debit discount is applicable for Payments made through any electronic mode through an auto debit mandate for 1st-year instalment.

Risk cover commences along with policy commencement for all lives, including minor lives.

Buying a Health Insurance Policy is a long-term commitment. An early termination of the Policy usually involves high costs, and the Surrender Value payable may be less than the all the Premiums Paid.

In case of non-standard lives and on submission of non-standard age proof, extra premiums will be charged as per our underwriting guidelines.

Discount on policy will be subject to sales literature and policy contract.

L&C/Advt/2026/Apr/2444

Cancer cover with 30-year fixed premiums

Upfront payout on cancer diagnosis

Explore BenefitsT&C apply