Call us

Call us

FOR EXISTING POLICY

FOR EXISTING POLICY

Have query on premium, payout or any servicing need?

Call us:

FOR NEW POLICY

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY (NRIs)

Note: Consent is provided to Tata AIA Life Insurance Company Limited to contact you by calling/giving missed call to the above numbers.

Thank you for sharing your details. To receive a call from Tata AIA Financial Advisor.

reCAPTCHA is not working.

No relevant search results found.

Get Life Cover of ₹1 Crore by paying a premium of

₹7,085/month

Total premium: ₹14.09 Lakh

Save ₹1,202 with discounts

Save ₹1,202 with discounts

Discounts

10% discount on 1st year premium is applicable on online purchase. This discount is auto-applied and can’t be removed

8.5% discount on 1st year premium is applicable for salaried personnel. You will need to share your corporate email ID if you opt for this discount. This discount is auto-applied if you select ‘Salaried’ as your occupation and can’t be removed

Applicable only if the policy is bought digitally. Some discounts will not be available when this option is selected.

1% discount on 1st year premium for all payments paid through any permissible electronic mode debited through an auto-debit mandate. Maximum discount capping: ₹100 over the year.

2% discount on 1st year premium on these milestones

| Event | Eligibility |

|---|---|

| Wedding (1 wedding only) | Within 6 months before or after the date of wedding |

| Birth/ Adoption of 1st child* | Within 6 months before or after the birth/ adoption date |

| Home loan | Within 6 months of loan getting sanctioned |

| First job | Within 6 months of joining date |

*Policy issuance eligibility for female customers will be determined by Board Approved Underwriting Policy (BAUP)

The above milestones cannot be clubbed to avail more discount, Such discount shall be capped to a maximum of ₹500 over the year.

Save up to 5% when you and a family member purchase policy together. Some discounts will not be available when this option is selected.

A certified Tata AIA expert will call you from a 1600‑series number to customize your plan.

Buy your plan

Please select an option

Minimum income: ₹5 Lakh

You opted for

Select details for the 2nd Policy

Select your relationship with the person you're buying this policy with.

Tata AIA Sampoorna Raksha Promise - Non-Linked, Non-Participating, Pure Risk, Individual Life Insurance Product (UIN:110N176V12)

Planning your future and that of your family is always a priority, and with the help of the right tools and solutions, achieving financial security can be simple. Life insurance is an important medium through which you can target multiple goals under a single life insurance policy.

With different types of life insurance plans to choose from, all you need to do is identify suitable policies for your family and yourself. And when the need arises, your policy will secure your needs adequately!

Our experts are happy to help you!

Why Do You Need Life Insurance?

It is true that no amount of money can replace the loss of life; however, if you are the sole earning member of your family, your death can result in a substantial loss of income for your loved ones. Life insurance addresses this loss of income during a time when your family cannot support themselves financially.

Apart from that, here are some important reasons why you need life insurance:

Protect Your Family’s Future

Fulfil Your Financial Objectives

Lead A Stress-Free Life

Retirement Planning

Life insurance is necessary and important for a number of reasons. Different policyholders have varying needs based on which life insurance can help them meet these objectives. Be it a simple life cover or a savings goal, given below is the importance of life insurance:

When you plan your savings and investment, a life insurance plan is an important part of your portfolio. If you want to save or invest through life insurance plans, a savings plan with guaranteed7 returns can be a low-risk investment. In addition, the premiums paid on your policy can be as per a frequency of your preference, just like a monthly or quarterly contribution.

Even if you do not need to save or invest through a life insurance policy, it is essential to secure your family’s future with a life insurance cover. Pure term plans that offer an extensive death benefit for affordable premiums can be a good choice to protect your loved ones during uncertain events or when you are no longer around to provide for your loved ones.

Apart from your savings funds, it is always advisable to have an emergency fund that can finance any emergency needs. This could be a medical contingency or a situation leading to the loss of income. A savings plan with assured returns can help you create and grow an emergency fund, which can help you and your loved ones in times of need.

Your life insurance premiums paid for the policy will qualify for tax6 deductions of up to ₹1.5 Lakh under Section 80C of the Income Tax Act, 1961, while the death benefits or maturity proceeds are exempt from tax under Section 10(10D). In addition, if you add a health rider to your life insurance policy, the rider5 premiums may qualify for tax benefits under Section 80D of the Income Tax Act.

Life insurance helps ensure that a family’s financial position does not collapse when income suddenly stops. It plays a key role in the following manner:

Choosing a life insurance policy is rarely about picking the “best” plan in isolation. It is more about what fits your financial reality and long-term responsibilities.

As the simplest form of life insurance, a term plan can offer a higher sum assured for your family’s needs, and you can pay very affordable premiums to keep the policy active. With the death benefit sum assured, your family can easily meet various financial goals in case of any unfortunate event such as death of life assured.

Know More about our Best-Selling Term Insurance Plan – Tata AIA Sampoorna Raksha Promise

Non-Participating, Non-Linked, Pure Risk Individual Life Insurance Product

(UIN: 110N176V12)

Non-Participating , Non-Linked, Pure Risk Individual Life Insurance Product

(UIN: 110N171V15)

The dual benefit of savings and life insurance under one policy with one premium can help you target and achieve complete financial protection for yourself and your family. In addition, the death or maturity benefits can sustain your family in your absence or help you meet your pre-planned future needs.

Know More about our Best-Selling Guaranteed Return Savings Plan

Non-Linked, Non-Participating, Individual Life Insurance Savings Plan

(UIN: 110N158V14)

Individual, non-linked, participating, Life Insurance Savings Plan (UIN: 110N207V02)

A Unit Linked Insurance Plan provides Market-linked returns^ can help you create wealth over the long term. Unit-Linked Insurance Plans are a unique combination of life insurance and investment, where you can choose the life cover and the funds you want to invest in. However, consider your risk profile before opting for a ULIP.

Know More About Our Unit Linked Insurance Plan

A pension or retirement plan is designed to offer a regular income stream to the insured and their family during retirement so that the absence of a monthly salary does not affect their lives. Additionally, the life cover can help sustain the retired insured’s family in case of an unfortunate event.

Know More About our Best-Selling Pension Plan – Tata AIA Smart Pension Secure

Non-Participating Unit Linked Individual Life Insurance Plan

(UIN: 110L182V09)

A Non-Linked, Non-Participating, Annuity Plan

(UIN:110N161V13) | T&C apply

Adequate Coverage

Choice of Policy

Life Insurance Provider

Additional Needs

Life insurance can serve multiple purposes, depending on your life insurance needs and the type of life insurance policy you choose. With multiple life insurance plans available, you must identify your life insurance needs and choose a policy that offers the required coverage to you and your loved ones in times of need.

Our experts are happy to help you!

A life insurance cover is designed to offer a life cover to your family basis the policy term chosen by you as per your life insurance needs. During this policy term, you, the policyholder, pay the life insurance premium to keep the policy active. In addition, if the life assured meets with an untimely demise during the life cover, your family will be offered a death benefit that will keep them financially secure even in your absence.

These are some of the important features of a life insurance policy:

A life insurance company issues a life insurance policy to a policyholder once the latter selects a policy as per their life insurance needs. Hence, it offers insurance coverage against the potential risk to one’s life.

In the event of the policyholder’s death during the policy term, the life insurance company will pay out the predetermined sum assured to the policyholder’s beneficiaries that will financially sustain them.

Life insurance is based on the following fundamental principles:

Purchasing life insurance has several benefits, such as offering financial assistance to the insured’s beneficiaries, helping one create and grow a wealth plan, enabling market-linked^ investment options along with a life cover, building a disciplined savings habit, retirement planning and much more.

A life insurance policy in India is offered to an insured by the insurer. In return for the life insurance cover, the insured has to pay the policy premiums regularly as per the predetermined premium paying term to keep the policy active and protect their family under the life insurance cover.

During the policy term, in case of the policyholder’s death, a predetermined sum assured will be paid out to the late policyholder’s beneficiaries to help sustain them financially.

Life insurance plans such as savings plans offer survival benefits and maturity benefits. Apart from the life insurance coverage for your family, a money-back savings plan can help you with a period payout benefit during the policy term. If you survive till the end of the policy term, the maturity benefits, which comprise the savings and any applicable bonuses, will be paid out.

People purchase a life insurance policy so that they can secure their families against life’s uncertainties. While many people may choose not to have a life insurance policy, at some point in time, you should consider creating a financial safety net for your family so that they can be financially secure in your absence.

Your claim is our priority. When you purchase a policy from Tata AIA Life Insurance, you claims will be settled within 4 hours~~.

~~T&C apply

Yes, life insurance plans enable you to choose a flexible policy term or policy tenure, depending on how many years of life insurance coverage you and your family need. In the case of whole life insurance plans, the coverage will be offered till the policyholder is 100 years* of age.

The life insurance plans you purchase will depend on your life insurance needs. Most people choose to start with a term insurance policy since the premiums are lower for younger policyholders. However, when you want to start saving or investing for your future, a savings policy or a unit-linked insurance plan can be a good choice.

If you are planning your retirement in your 40s or 50s, then during those years, you can purchase a retirement plan that will offer a steady source of income for you and your family retirement.

Though life insurance does offer tax# benefits under the prevailing tax laws, the primary goal of a life insurance policy is to offer a life insurance cover to your family. This life cover will support your loved ones financially in case of your death during the policy term.

The claim settlement ratio is an important indicator of a life insurance provider’s capacity to settle your claims in full and on time. If your life insurance provider has a high claim settlement ratio, it means they have settled many claims during a financial year against the number of claims received.

The premium payment frequency in life insurance policy plans is the number of times you can pay your premiums in a year. Hence, if you choose the monthly frequency, you pay your premium each month and so on. Hence, you can pay your life insurance premiums annually, half-yearly, quarterly, or monthly.

If you have opted for a life insurance policy that does not offer a return of premiums, you cannot receive the life insurance premiums back as a maturity benefit. However, life insurance plans with a return of premium benefit will pay the total of all the paid life insurance premiums to you at the end of the policy term if a death claim has not been filed.

Popular Searches

Disclaimer

The linked insurance product do not offer any liquidity during the first five years of the contract. The policy holder will not be able to surrender/withdraw the monies invested in linked insurance products completely or partially till the end of the fifth year.

Tata AIA Sampoorna Raksha Promise - Non-Linked, Non-Participating, pure risk, Individual Life Insurance Product (UIN:110N176V12)

Tata AIA Maha Raksha Supreme Select - Non-Linked, Non-Participating, Pure Risk, Individual Life Insurance Product (UIN: 110N171V15)

The complete name of Tata AIA Fortune Guarantee Plus is Tata AIA Life Insurance Fortune Guarantee Plus (UIN: 110N158V14) - Non-Linked, Non-Participating, Individual Life Insurance Savings Plan.

Tata AIA Shubh Flexi Income Plan (UIN: 110N207V02) - Individual, Non-Linked, participating, Life Insurance Savings Plan

Param Raksha Life Pro+ is designed for combination of benefits of following individual and separate products named (1) Tata AIA Smart Sampoorna Raksha Supreme Unit Linked, Non-Participating Individual Life Insurance Plan (UIN: 110L179V02) and (2) Tata AIA Health Buddy, Non-Participating, Non-Linked, Individual Health Product (UIN: 110N183V01). Both Smart Sampoorna Raksha Supreme and Tata AIA Health Buddy are also available for sale individually.

Tata AIA Premier SIP is a combination of the Tata AIA Smart SIP, a non-participating, unit-linked, individual life insurance savings plan (UIN: 110L174V02), and Tata AIA Health Buddy, Non-Participating, Non-Linked, Individual Health Product (UIN: 110N183V01). Both Tata AIA Smart SIP and Tata AIA Health Buddy are also available for sale individually.

Tata AIA Smart Pension Secure (UIN: 110L182V09) - Non-Participating, Unit Linked, Individual Life Insurance Pension Plan

The complete name of Tata AIA Fortune Guarantee Pension Plan is Tata AIA Life Insurance Fortune Guarantee Pension Plan (UIN:110N161V13) - A Non-Linked Non-Participating Individual Life Insurance Plan

1As per the duly approved product design and terms & conditions of the product, illustrated premium of ₹501 is the monthly premium for a 20 yr. old female, Standard Life, Non-Smoker for ₹1 Cr. Sum Assured with Policy Term of 20 yrs. (Regular Pay) under Life Promise Option of Tata AIA Sampoorna Raksha Promise with first year premium discount of 10% for digital purchase and 8.5% for salaried person. Please refer Benefit Illustration for more details.

2As per the duly approved product design and terms & conditions of the product, this includes first year digital discount of 10% for Limited Pay/Regular Pay and 8.5% salaried discount. For Single Pay, 1% discount will be available for online purchase and salaried discount each.

3Under Life Promise Plus Option, an amount equal to the 100% of the Total Premiums Paid (excluding loading for modal premiums) shall be payable at the end of the Policy Term, provided the life assured survives till maturity and the policy is not terminated earlier.

4Applicable to only non-early claims with more than 3 years of policy duration, non-investigation cases, up to Sum Assured of ₹50 Lakh. Applicable for branch walk in. Time limit to submit claim to Tata AIA Life Insurance is 2 pm on working days. Subject to submission of complete documents. Not applicable for ULIP policies and open title claims.

5Rider is not mandatory and is available for a nominal extra cost. For more details on benefits, premiums, and exclusions under the Rider, please contact Tata AIA Life's Insurance Advisor/ branch.

6Income Tax benefits would be available as per the prevailing income tax laws, subject to fulfilment of conditions stipulated therein. Income Tax laws are subject to change from time to time. Tata AIA Life Insurance Company Ltd. does not assume responsibility on tax implication mentioned anywhere in this document. Please consult your own tax consultant to know the tax benefits available to you

No Goods and Service Tax shall be applicable on Individual life insurance products as per prevailing laws. Tax laws are subject to amendments from time to time. If any imposition (tax or otherwise) is levied by any statutory or administrative body under the Policy, Tata AIA Life Insurance Company Limited reserves the right to claim the same from the Policyholder.

7Guaranteed Income shall be total of Guaranteed annual Income plus Income Booster payable in a year. Guaranteed Income as per the chosen Income Frequency shall commence after maturity till the end of the Income Period, irrespective of survival of the life insured(s) during the Income Period.

8Return of Premium shall be the sum of Guaranteed Maturity Benefit plus Milestone Benefit and shall be payable at the end of the Income Period, irrespective of survival of the life insured(s) during the Income Period.

9Available under Regular Income with an Inbuilt Critical Illness Benefit option

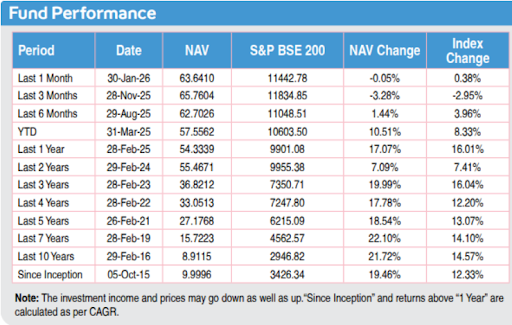

105-year computed NAV for Multi Cap Fund as of February 2026. Other funds are also available. Benchmark of this fund is S&P BSE 200

Some benefits are guaranteed and some benefits are variable with returns based on the future performance of your insurer carrying on life insurance business. If your policy offers guaranteed benefits then these will be clearly marked “guaranteed’. If your policy offer variable benefits then it will show two different rates of assumed future investment returns. These assumed rates of return are not guaranteed and these are not the upper or lower limits of what you might get back, as the value of your policy is dependent on a number of factors including actual future investment performance

11All funds open for new business which have completed 5 years since inception are rated 4 star or 5 star by Morningstar as of August 2025.

©2025 Morningstar. All rights reserved. The Morningstar name is a registered trademark of Morningstar, Inc. in India and other jurisdictions. The information contained here: (1) includes the proprietary information of Morningstar, Inc. and its affiliates, including, without limitation, Morningstar India Private Limited (“Morningstar”); (2) may not be copied, redistributed or used, by any means, in whole or in part, without the prior, written consent of Morningstar; (3) is not warranted to be complete, accurate or timely; and (4) may be drawn from data published on various dates and procured from various sources and (5) shall not be construed as an offer to buy or sell any security or other investment vehicle. Neither Morningstar, Inc. nor any of its affiliates (including, without limitation, Morningstar) nor any of their officers, directors, employees, associates or agents shall be responsible or liable for any trading decisions, damages or other losses resulting directly or indirectly from the information.

13Illustrated Premium of ₹679 is the monthly premium for 20 yr. old female, Standard Life, Non-Smoker for 2 Cr. Sum Assured with Policy Term of 20 yrs. (Regular Pay) with Life Secure plan option of Tata AIA Maha Raksha Supreme Select with first year premium discount for digital purchase and salaried person.

14Inbuilt Payout Accelerator Benefit pays out 50% of Effective Sum Assured opted in case of a Terminal Illness diagnosis

16Return of Purchase price means return of all premiums paid excluding any extra premium, any rider premium, taxes and other statutory levies, if applicable.

Risk cover commences along with policy commencement for all lives, including minor lives. Buying a Life Insurance Policy is a long-term commitment. An early termination of the Policy usually involves high costs, and the Surrender Value payable may be less than the all the Premiums Paid. In case of non-standard lives and on submission of non-standard age proof, extra premiums will be charged as per our underwriting guidelines. All Premiums and interest payable under the policy are exclusive of applicable taxes, duties, surcharge, cesses, or levies which will be entirely borne/ paid by the Policyholder, in addition to the payment of such Premium or interest. Tata AIA Life shall have the right to claim, deduct, adjust, and recover the amount of any applicable tax or imposition, levied by any statutory or administrative body, from the benefits payable under the Policy.

The risk factors of the bonuses projected under the product are not guaranteed.

Past performance doesn't construe any indication of future bonuses.

These products are subject to the overall performance of the insurer in terms of investments, management of expenses, mortality and lapses.

For more details on risk factors, terms and conditions please read sales brochure carefully before concluding a sale.

Linked Life Insurance products are different from traditional insurance products and are subject to risk factors.

The premium paid in Unit Linked Life Insurance policies are subject to investment risks associated with capital markets and the NAVs of the units may go up or down based on the performance of fund and factors influencing the capital market and the insured is responsible for his/her decisions.Various funds offered under this contract are the names of the funds and do not in any way indicate the quality of these plans, their future prospects and returns. The premium paid in Linked Life Insurance policies is subject to investment risks associated with capital markets and publicly available index. The NAV of the units may go up or down based on the performance of Fund and factors influencing the capital market/publicly available index and the insured is responsible for his/her decisions. On survival to the end of the policy term, the Total Fund Value including Top-Up Premium Fund Value valued at applicable NAV on the date of Maturity will be paid

Investments are subject to market risks. The Company does not guarantee any assured returns. The investment income and price may go down as well as up depending on several factors influencing the market

Tata AIA Life Insurance Company Limited is only the name of the Life Insurance Company & Tata AIA Smart SIP, Tata AIA Smart Sampoorna Raksha Supreme, Tata AIA Smart Pension Secure, is only the name of the Linked Insurance contract and does not in any way indicate the quality of the contract, its future prospects or returns.

The investment income and price may go down as well as up depending on several factors influencing the market. Please know the associated risks and the applicable charges, from your insurance agent or the Intermediary or policy document issued by the insurance company. Please make your own independent decision after consulting your financial or another professional advisor. Returns are calculated on an absolute basis for a period of less than (or equal to) a year, with reinvestment of dividends (if any). All investments made by the Company are subject to market risks. The Company does not guarantee any assured returns

The performance of the managed portfolios and funds is not guaranteed, and the value may increase or decrease in accordance with the future experience of the managed portfolios and funds

Various funds offered under this contract are the names of the funds and do not in any way indicate the quality of these plans, their future prospects and returns. Premium paid in Unit Linked Life Insurance policies are subject to investment risks associated with capital markets and the NAVs of the units may go up or down based on the performance of fund and factors influencing the capital market and the insured is responsible for his/her decisions.

Past performance is not indicative of future performance. Returns are calculated on an absolute basis for a period of less than (or equal to) a year, with reinvestment of dividends (if any)

If your policy offers variable benefits, then the illustrations on this page will show two different rates of assumed future investment returns. Currently the gross investment returns are stipulated as 4% p.a. and 8% p.a. These assumed rates of return are not guaranteed, and these are not the upper or lower limits of what you might get back, as the value of your policy is dependent on a number of factors including actual future investment performance.

Life insurance cover is available under the solution. For more details on risk factors, terms and conditions please read Sales Brochure carefully before concluding a sale.

Buying a Life Insurance Policy is a long-term commitment. An early termination of the Policy usually involves high costs, and the Surrender Value payable may be less than the all the Premiums Paid.

In case of non-standard lives and on submission of non-standard age proof, extra premiums will be charged as per our underwriting guidelines

L&C/Advt/2026/Jun/3940