No relevant search results found.

Language

Thank you for sharing your details. To receive a call from Tata AIA Financial Advisor.

reCAPTCHA is not working.

Call us

FOR EXISTING POLICY

FOR EXISTING POLICY

FOR NEW POLICY

FOR NEW POLICY

Want to buy a new policy online?

Term Insurance Calculator

Your premium calculation is in progress

What is Term Insurance Calculator?

A term insurance calculator is a free online tool that can be used to give premium estimates for a term insurance plan. It is primarily used to compare term policy quotes under different benchmarks. The inputs such as age, gender, income, etc., are utilized to gauge the policy amount, premium and term insurance plan best suited for you.

How Does a Term Insurance Calculator Work?

Here is a step-by-step explanation of how Tata AIA's term policy calculator works:

- Enter Information

You start by entering information into the provided fields like name (legal first and last name), date of birth, gender, contact details (mobile number), and other details so that we can suggest you the right plan for you.

- Coverage Estimation

Based on your input and risk assessment, the term life insurance calculator will estimate the coverage amount needed to cover your financial goals and dependents in case of any unfortunate events. You can change the coverage amount, premium term and policy term to check the premium amount.

- Premium Calculation

The calculator will estimate the premium amount needed to pay for the desired coverage. You can add additional riders4 to increase the plan coverage.

- Comparison

Term insurance calculators in India allow you to compare quotes from term plans to find the best policy at a competitive price tailored to your needs. At Tata AIA, our term plan calculator will allow you to compare quotes for different variations under the same term policy based on your input.

- Customization

Since term plan calculators give you real-time estimates, you can continue to adjust the coverage amount, policy length, add-on features and other parameters to see how they impact your premium.

- Results

Using all the data you have provided; the term insurance calculator will give an estimated premium for your desired term insurance policy. This will bring financial clarity and help you make an informed decision about buying a Tata AIA term plan that aligns with your financial goals and budget.

Our Best Selling Term Insurance Plans

Non-Linked, Non-Participating, Pure Risk, Individual Life Insurance Product (UIN:110N176V05)

Non-Linked, Non-Participating, Pure Risk, Individual Life Insurance Product (UIN: 110N171V08)

Why choose a term plan?

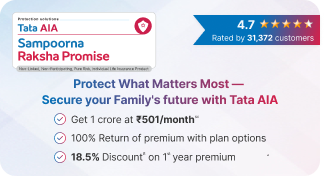

Our bestselling term plan – Tata AIA Sampoorna Raksha Promise

Plan options in Sampoorna Raksha Promise

| Life Promise | Life Promise Plus | |||

| Entry Age (Years) | Minimum | Maximum | Minimum |

Maximum |

| 18 years | 65 years | 18 years | 65 years | |

| Maturity Age (Years) | Minimum |

Maximum | Minimum |

Maximum |

| 18 years | 100 years | 28 years | 100 years | |

| Pay Premium For (Premium Payment Term in Months) |

Minimum |

Maximum | Minimum |

Maximum |

|

|

|

|

|

| Stay Covered For (Policy Term in Months) |

Minimum | Maximum | Minimum |

Maximum |

|

|

|

|

|

| Life Cover Amount (Base Sum Assured in ₹) |

Minimum |

Maximum | Minimum |

Maximum |

| 25 lakhs | No Limit (Subject to Board approved underwriting policy (BAUP)) |

25 lakhs | No Limit (Subject to Board approved underwriting policy (BAUP)) |

|

| Premium Payment Mode | Single Pay Annual Semi-annual Quarterly Monthly |

Single Pay |

||

| Death Benefit | Highest of:

|

Highest of:

|

||

| Option To Cover till Age Of 100 (Whole Life Coverage)10 |

Yes |

Yes |

||

| Option To Get Your Premium Amount** Back | No |

Yes |

||

| Increase Life Cover at Important Milestones* such as Marriage/Childbirth/home loan/First Job | Available |

Available |

||

| Terminal Illness Cover | No |

Payor accelerator benefit is payable on confirmed diagnosis of terminal illness of the life assured |

||

| Health Benefit | Available with Riders |

Available with Riders |

||

| Income Benefit | No |

No |

||

| Tax Benefit Up to Rs. 46,8009 | Yes |

Yes |

||

| Upfront Premium Discount8 | discount of 1% of single premium or 5% on First year premiums for regular and limited pay. |

discount of 1% of single premium or 5% on First year premiums for regular and limited pay. |

||

| Life Promise | Life Promise Plus | ||

|---|---|---|---|

| Entry Age (Years) | |||

| Minimum | Maximum | Minimum | Maximum |

| 18 years | 65 years | 18 years | 65 years |

| Maturity Age (Years) | |||

| Minimum | Maximum | Minimum | Maximum |

| 18 years | 100 years | 28 years | 100 years |

| Pay Premium For (Premium Payment Term in Months) |

|||

| Minimum | |||

|

|

||

| Maximum | |||

|

|

||

| Stay Covered For (Policy Term in Months) |

|||

| Minimum | |||

|

|

||

| Maximum | |||

|

|

||

| Life Cover Amount (Base Sum Assured in ₹) |

|||

| Minimum | |||

25 lakhs |

25 lakhs |

||

| Maximum | |||

|

No Limit

(Subject to Board approved underwriting policy (BAUP)) |

No Limit

(Subject to Board approved underwriting policy (BAUP)) |

||

| Premium Payment Mode | |||

|

Single Pay: Annual / Half-yearly / Quarterly / Monthly

|

|||

| Death Benefit | |||

Highest of: |

Highest of: |

||

| Option To Cover till Age Of 100 (Whole Life Coverage) |

|||

Yes |

Yes |

||

| Option To Get Your Premium Amount** Back | |||

No |

Yes |

||

| Increase Life Cover at Important Milestones such as Marriage/Childbirth/home loan/First Job |

|||

Available |

Available |

||

| Terminal Illness Cover | |||

No |

Payor accelerator benefit is payable on confirmed diagnosis of terminal illness of the life assured |

||

| Health Benefit | |||

Available with Riders |

Available with Riders |

||

| Income Benefit | |||

No |

No |

||

| Tax Benefit Up to Rs. 46,8009 | |||

Yes |

Yes |

||

| Upfront Premium Discount | |||

Discount of 1% of single premium or 5% on First year premiums for regular and limited pay. |

Discount of 1% of single premium or 5% on First year premiums for regular and limited pay. |

||

Sample Illustration$$

₹1 Crore Term Plans

Life Promise

1 crore Life cover | Standard Life | Non-Smoker | 20 years Premium Payment term | Regular pay | Life Option

| Age | Monthly Premium | Annual Premium | ||

|---|---|---|---|---|

| Male | Female | Male | Female | |

| 20 years | ₹589 | ₹501 | ₹6,672 | ₹5,671 |

| 30 years | ₹759 | ₹645 | ₹8,592 | ₹7,303 |

| 40 years | ₹1,288 | ₹1,094 | ₹14,583 | ₹12,395 |

Life Promise Plus

1 crore Life cover | Standard Life | Non-Smoker | 20 years Premium Payment term | Regular pay | Life option| Premium with Return of Premium

| Age | Monthly Premium | Annual Premium | ||

|---|---|---|---|---|

| Male | Female | Male | Female | |

| 20 years | ₹1406 | ₹1,195 | ₹15,921 | ₹13,533 |

| 30 years | ₹2,042 | ₹1,735 | ₹23,123 | ₹19,654 |

| 40 years | ₹3,997 | ₹3,957 | ₹45,265 | ₹38,475 |

Life Promise

2 crore Life cover | Standard Life | Non-Smoker | 20 years Premium Payment term | Regular pay | Life Option

| Age | Monthly Premium | Annual Premium | ||

|---|---|---|---|---|

| Male | Female | Male | Female | |

| 20 years | ₹946 | ₹804 | ₹10,709 | ₹9,101 |

| 30 years | ₹1,275 | ₹1,083 | ₹14,436 | ₹12,270 |

| 40 years | ₹2,348 | ₹1,995 | ₹26,586 | ₹22,597 |

Life Promise Plus

2 crore Life cover | Standard Life | Non-Smoker | 20 years Premium Payment term | Regular pay | Life option| Premium with Return of Premium

| Age | Monthly Premium | Annual Premium | ||

|---|---|---|---|---|

| Male | Female | Male | Female | |

| 20 years | ₹2,042 | ₹1,736 | ₹23,130 | ₹19,660 |

| 30 years | ₹3,041 | ₹2,585 | ₹34,437 | ₹29,270 |

| 40 years | ₹6,482 | ₹5,510 | ₹73,412 | ₹62,400 |

Life Promise

3 crore Life cover | Standard Life | Non-Smoker | 20 years Premium Payment term | Regular pay | Life Option

| Age | Monthly Premium | Annual Premium | ||

|---|---|---|---|---|

| Male | Female | Male | Female | |

| 20 years | ₹1,364 | ₹1,159 | ₹15,451 | ₹13,131 |

| 30 years | ₹1,857 | ₹1,579 | ₹20,034 | ₹17,877 |

| 40 years | ₹3,504 | ₹2,978 | ₹39,679 | ₹33,725 |

Life Promise Plus

3 crore Life cover | Standard Life | Non-Smoker | 20 years Premium Payment term | Regular pay | Life option| Premium with Return of Premium

| Age | Monthly Premium | Annual Premium | ||

|---|---|---|---|---|

| Male | Female | Male | Female | |

| 20 years | ₹2,934 | ₹2,494 | ₹33,226 | ₹28,240 |

| 30 years | ₹4,390 | ₹3,731 | ₹49,716 | ₹42,258 |

| 40 years | ₹9,550 | ₹8,117 | ₹1,08,154 | ₹91,930 |

Premiums given are excluding taxes

Enhance your coverage with riders

Non-Linked, Non-Participating, Pure Risk, Individual Life Insurance Product (UIN:110N176V05)

Non-Linked, Non-Participating, Pure Risk, Individual Life Insurance Product (UIN: 110N171V08)

Non-Linked, Non-Participating, Pure Risk, Individual Life Insurance Product (UIN: 110N171V08)

Why choose Tata AIA Life Insurance?

Factors that Determine Term Insurance Premium

- Insurance Requirements

Your expected requirements under a term plan play a significant role in determining your overall premium rate. These can vary depending on what stage of life you are in. Hence, different term plans will cater to different needs. For example, an increasing term plan will account for changing factors like inflation or increased living costs, a decreasing term plan can be used to cover the years needed to pay off a loan, etc.

- Age

Younger individuals are charged lower term insurance premiums than older policyholders. This is because the younger you are, the less risk you pose or the less likely you are to develop serious health conditions. In other words, the same term plan will charge you a higher premium for the same coverage at an older age vs when you are younger. Premium rates under term plans also stay the same throughout the policy’s term. Hence, we recommend buying one early to maintain a low-cost insurance cover over a longer tenure.

- Coverage Amount

The higher the sum assured, the higher your premiums. Generally, the minimum sum assured should be at least 15 - 20 times your annual income. This is because the term plan's sum assured should be enough to cover the needs of ALL your dependent family members. You should account for current living expenses, future needs, inflation rates, emergency expenses, any existing liabilities and other financial obligations to ensure you pick the right amount for a death benefit payout.

- Policy Term

The longer the duration of your policy coverage, the lesser your premium rates. Hence, if you are looking for cost-efficiency, we recommend going for a long-term policy. If you are unsure how long you will need term insurance coverage, assessing your financial goals and existing liabilities can point you in the right direction. Moreover, at Tata AIA, we offer several term plans with a life cover option to ensure coverage up to 100 years of age.

- Medical History

Your current health condition, i.e., whether you have a pre-existing illness, can affect your overall premium rates. This is because critical illnesses like cancer can increase the likelihood of premature death, thereby increasing your risk as a candidate. Always disclose any information regarding this factor honestly to the insurance agent, as hiding the fact that you have a pre-existing condition may violate policy terms, resulting in your family members being unable to claim the death benefit.

- Lifestyle

Term insurance calculators in India may require you to enter lifestyle information like smoking status or alcohol consumption. For example, Tata AIA's term insurance plan calculator requires you to provide your smoking status. Certain lifestyle choices can increase your risk of developing health conditions, as a result, increasing your premium rates. This means individuals of the same age and gender with good lifestyle practices are charged lower premiums.

- Occupation

Some insurers will charge candidates who work in relatively high-risk jobs like police officers, firefighters, miners, etc., a higher premium since these jobs increase their risk profile. Your occupation may not significantly affect overall premiums, but it is something to keep in mind when applying for a term insurance plan or calculating premiums. In most cases, annual income and income proof are more important to an insurer, as they will determine your ability to pay for premiums.

- Gender

Term policy calculators’ factor in your gender when calculating premiums, as some insurers offer women lower premium rates. The price difference between genders is not big enough to significantly impact the overall cost, but it still factors into the overall calculation. Women often lead longer lives than men and may require long-term coverage. At Tata AIA, we also offer preferential premium rates for women.

How Can a Term Insurance Calculator Help You?

A powerful tool, a term insurance calculator helps you understand what premiums you have to pay and what coverage you can expect. It can help you in many ways. Some of these are:

- Finds the Right Coverage:

It goes ahead and calculates the ideal sum assured by keeping in mind different factors like your income, liabilities, lifestyle, and future goals. This is done to ensure your family is well covered and has financial security.

- Helps You Compare Plans:

You can check different premium amounts for various coverage options, helping you find the most cost-effective plan.

- Budget-Friendly Premium Estimates:

By changing the term of the policy, coverage amount, and riders, you can modify your policy to suit your budget.

- Saves Time & Effort:

No need for manual calculations—just enter your details, and the calculator provides instant estimates.

- Rider Benefit Analysis:

You can see how add-ons like critical illness cover or accidental death benefit impact your premium.

Using a term insurance calculator ensures you make an informed decision, selecting a plan that meets your needs without overpaying. It’s a quick and hassle-free way to secure your family’s financial future with the right protection.

Benefits of a Term Plan Premium Calculator

- Quick and Convenient:

You are not required to present any documents or go through any additional processes to get your premium estimates when using a term plan calculator. Once you have your quotes, you can immediately buy your Tata AIA term plan.

- Accurate Quotes:

You get accurate and real-time estimates based on current inflation rates and other changing factors. This means you will know exactly how much your term policy will cost based on your current insurance requirements.

- Allows for Better Financial Planning:

Since term insurance calculators offer accurate estimates and premiums stay the same throughout the policy term, you know exactly how much money to set aside to pay for your term plan. Thus, allowing for better financial planning.

- Free and Cost-Effective:

This is a free tool offered by online insurers that anyone can use. Hence, using this tool in tandem with your online term policy purchase can allow you to easily access discounts and lower premium rates, helping you save money in the long run.

- Generic

- Policy

- Cover

- Premium

- Claim

1.Why use a term insurance calculator?

A term insurance calculator should be used since it is a quick, simple and free-of-cost way to calculate your term insurance premium.

2.How to use a Tata AIA’s term insurance calculator?

Here is a step-by-step process on how to use Tata AIA's term plan calculator:

Enter Your Details

- Enter your details in the given fields like name (Legal first and last name), date of birth, gender, smoking status and a valid phone number.

- Click 'Calculate Premium' and enter the OTP sent to your phone number via text message.

- You will be redirected to a page where you provide more details like your annual income and occupation (income type). Click Next.

Choose Your Sum Assured and Policy Term

- On this page, you will be provided multiple quotes for different variations of your chosen term plan. Here, you can choose your sum assured amount from the given options, your policy term and the premium payment modes and terms.

Opt for or Omit Add-Ons and/or Additional Features Under the Term Plan

- On the same page, you can opt in or out of additional features available under the term plan. These include life cover (up to 100 years)7, Return of Premium (ROP)~ maturity benefit and other add-ons. Remember. These come with an additional cost.

Compare Your Options

- Once you are done customizing your plan, you can now compare your premium rates under different quotes. This will allow you to buy the best Tata AIA term insurance plan for you and your family.

3.Can I purchase a term plan online?

Yes, you can purchase a term plan online by visiting the Tata AIA Life Insurance official website and going to the Buy Online section. Once you select a term plan of your choice, you can buy the plan and make the payment online in a few easy steps.

4.Why is a term plan important?

A term plan is important because it offers comprehensive life cover protection to your family at very affordable premiums. In case of an unforeseen eventuality, the sum assured will financially support your family so that they can sustain themselves.

5.Can I have different life insurance plans along with a term plan?

Yes, you can have different life insurance plans as well as a term plan based on your and your family’s insurance needs.

6.What are the three main advantages of having term insurance?

Though term insurance offers multiple benefits, here are the three primary benefits of term plans:

- Simple and easy to understand

- High Sum assured at comparatively Affordable premiums

- Flexible policy terms and premium paying terms allowing customization based on needs

7.What is the right age to stop term life insurance?

The aim of term insurance is to ensure the financial security of your family in the event of your untimely demise with a death benefit. Hence, if you have a term plan for a certain policy term, it is advisable to continue the insurance coverage until the end of the selected policy term.

8.How can one select the best term insurance plan?

The most suitable term plan would be the one that can be customised as per your needs, after you evaluate all your requirements based on your lifestyle, family’s needs, liabilities and debts and other emergency needs. You also consider your premium payment capacity so that you are able to pay the premiums on time and avail of the life insurance coverage.

9. Can I safely purchase term insurance online?

Yes, you can safely buy term insurance online when you buy a term plan from the official website of Tata AIA Life Insurance.

10. What are the different types of life insurance plans?

The different types of life insurance plans are as given below:

- Term Insurance

- Term Insurance with Return of Premium

- Term + Wealth Plans

- Savings Plans

- Child Insurance Plans

- Whole Life Insurance Plans

- Endowment Insurance Plans

- Unit-Linked Insurance Plans (ULIPs)

- Retirement Plans

- Money Back Insurance Plans

- Group Insurance

- Combo Plans

11.What is the Married Women's Property (MWP) Act, and who is it useful for?

The Married Women's Property (MWP) Act safeguards married women's property rights. It enables married women to own and control property in their name rather than having their property automatically become their husband's property upon marriage.

If you purchase a term insurance plan under the MWP Act, the death benefits will only be paid out to your wife or wife + children in case of multiple beneficiaries. Thus, you can ensure that no one apart from your wife or children can access the death benefits of the term policy.

12.Who can be added as a beneficiary under the MWP Act?

The beneficiaries you can add to a term insurance policy under the MWPA can be your wife, your child/children, or your wife + children.

You can assign a certain percentage of the sum assured to each beneficiary or divide it into equal parts.

13.How much tax can I save with a term plan?

You can claim up to ₹1.5 Lakh in the form of tax8 deductions on your term insurance premiums each year under Section 80C of the Income Tax Act. Also, the beneficiary amount is tax deductible under Section 10(10D)

14.What are the tax benefits on the death benefit of my term plan?

The death benefit of your term insurance plan, payable to your beneficiaries on death, is exempt from tax under Section 10(10D) of the Income Tax Act.

1.What are the popular Tata AIA Life Insurance term plans?

Tata AIA offers 5 distinct term insurance plans under its catalogue:

- Tata AIA Sampoorna Raksha Promise - Non-Linked, Non-Participating, pure risk, Individual Life Insurance Product (UIN:110N176V05)

- Tata AIA Maha Raksha Supreme Select - Non-Linked, Non-Participating, Pure Risk, Individual Life Insurance Product (UIN: 110N171V08)

You can opt for coverage among any of these term plans to ensure your family stays protected in your absence. If you are uncertain about what term plan to choose, feel free to use our term insurance calculator to compare quotes and policy benefits.

2.Are all the term plans the same?

No, all term plans do not have the same offerings. For example, some term plans only offer pure protection while others offer a return on the premium. Some other term plans can also offer a life cover along with an income option.

Depending on the plan, you can choose the duration of the coverage, the premium payment term and the option to increase the coverage if needed

3.Is a term insurance calculator the same as other life insurance calculators?

No, a term plan premium calculator is not the same as other life insurance calculators. For instance, a ULIP calculator will show you the estimated returns you can receive on your policy, while a term insurance plan will show you the sum assured and coverage your family can receive and the premium required for the same.

4.What will happen if my nominee passes away before me?

If your term policy nominee passes away before you, the proceeds of your term life insurance policy will be paid to the beneficiary designated in your policy.

If your term policy nominee passes away before you, the proceeds of your term life insurance policy will be paid to the beneficiary designated in your policy.Therefore, in such a scenario, you should select a new nominee. You can contact us if you have concerns about your term life insurance policy or beneficiary designation.

5. Will I get the same benefits on a term plan as any other form of life insurance in India?

No, the benefits offered by a term plan are different from other life insurance plan benefits. For example, a savings plan will enable you to save a financial corpus, while a term plan offers extensive life cover benefits for your family.

6.Can the nominee be changed after I have purchased the policy?

.Yes, You can change the nominee in term insurance after purchasing the policy. You can contact us if you want to change the nominee in your policy, and we will assist you with the process and the necessary documentation.

7.Can pregnant women purchase a term policy?

Yes, pregnant women can purchase a term insurance policy, subject to certain policy terms and conditions.

8. Can housewives purchase a term policy?

Yes, housewives can purchase a term plan based on their family’s needs. You can calculate reasonable premiums of your choice using our term insurance calculator. This can help you pay affordable premiums while protecting your family.

9. Are there any special advantages available for women?

Tata AIA term insurance plans offer preferential premium rates to women policyholders than their male counterparts.

1. What types of deaths are covered in term plans?

Term plans cover most forms of death; however, they do have specific guidelines on suicide and self-inflicted injuries.

Generally, most insurers only cover suicide after the first 12 months from policy commencement. For any deaths due to suicide before this time frame, the insurance company will only pay the policy nominee 80% of the premiums paid during the first year.

Term plans cover most forms of death; however, they do have specific guidelines on suicide and self-inflicted injuries. If you want to know policy-specific guidelines on how we handle claims for death due to suicide under your chosen plan, feel free to contact us.

2. What benefits does a term plan offer?

A pure term plan offers a death benefit to the family of the policyholder in the event of the latter’s untimely death during the policy year and no maturity benefits. However, a return of premium term plan offers a 100% return on the premiums~ if the policyholder survives the term.

3. Can I add riders to my term plan?

Yes, you can add riders to your term insurance plan depending on the type of situation you need additional coverage for. You can get a critical illness rider and receive coverage when diagnosed with a critical illness covered under the rider. Or you can get a waiver of premium cover and have future premiums on your policy waived off in case of permanent and total disability or other conditions as stated under the rider6

4. How many riders do I add to my term plan?

The number of riders you add to your term plan will be based on your need. However, additional riders mean an additional premium, and so, to keep your premium payments in check, choose only the riders6 you deem necessary.

5.Will I need to mention medical details on a term insurance calculator?

No, the Tata AIA Life Insurance term insurance calculator does not need your medical tests or reports..

6.How to get the best term insurance coverage?

To choose the best term insurance coverage, be sure to analyse your insurance needs, research all term plans, use a term insurance premium calculator to calculate the premiums. You can then choose a policy that suits you and your family well based on the coverage and the premiums.

7. What type of deaths are covered in term plans?

Term plans cover all types of death; however, there may be specific guidelines regarding death by suicide. If you need additional life insurance coverage for your family in case of accidental death, you can add an accidental death benefit rider or a similar rider to your term plan.

8. What is the maximum cover I can get for a term plan without providing medical documents?

When you buy a term plan from Tata AIA Life Insurance, you need not provide any medical documents. You also need not undergo any medical check-ups before buying the term policy if you are young and do not have any potential health conditions. However, this requirement may be subject to the company’s terms and conditions and plan eligibility.

9. What is a lump sum payout, and who should choose it?

A lump sum payout is a benefit payout mode selected by you (the policyholder). This means the death benefit proceeds of the term plan will be paid out as a single lump sum amount to your beneficiaries on your death.

Lump sum payouts can be a good option if your family needs a large sum of money immediately, such as to pay off debts or to buy a house soon for better financial security.

10. What is a monthly income plan, and who should choose it?

A monthly income plan is a regular income option under a term insurance policy. This payout mode allows your beneficiary to receive the death benefit in monthly payments rather than as a lump sum.

These payments can provide a steady income over a longer period, which is helpful if your family cannot invest a large sum of money. Monthly income plans can also be suitable if your family needs a consistent source of income to cover ongoing expenses, such as mortgage payments or living expenses.

1. Will I get the right premiums with a term insurance calculator?

Term insurance calculators provide instant and accurate estimations and quotes based on your input. They are extremely reliable and mitigate the chances of human errors occurring during calculations as well.

To ensure you get relevant estimates under your chosen policy, make sure your details are correct and up to date.

2. Can I use a term insurance calculator while renewing my term plan?

The use of a term insurance calculator is best before you purchase a term insurance policy, as you cannot adjust your premium payments when renewing your term plan.

3. Can I increase or decrease my premium amount on the calculator?

Yes, you can adjust the premium amount on the calculator by changing some of the variables on the calculator. However, do remember to provide the right details so that you can get accurate term insurance premium quotes.

4. Will my premiums increase if I purchase a term plan close to retirement?

Yes, the older you get, the higher your premiums will be. Hence, when you are close to retirement, your premiums will be higher than when you first started working.

5. Will my term plan lapse if I don’t make a premium payment?

Premiums need to be paid by the due date to keep the policy active. Most policies have an additional grace period to pay due premiums without affecting the policy benefits. The grace period can be 15 days or 30 days, depending on the mode of the policy purchase. The policy may lapse or be converted to a reduced paid-up policy (depending on the terms and conditions of the policy) if the premiums are not paid within the grace period.

6.How much premium should one pay for 1 crore term insurance?

With the help of a term insurance calculator, you can easily calculate the premium amount for your 1 crore term insurance. The calculator will help you choose a policy term and a premium paying term that enables you to pay affordable premiums.

7. How is the term life insurance premium amount computed?

Your term life insurance premium will be calculated on the basis of your age, your health, your family’s medical history, your lifestyle habits, your profession, and any other factors that may pose a risk to your health. When you use a term plan premium calculator, these factors will be considered when the calculator determines your premium amount.

8. How does your age affect your term plan premium?

When you are young, you are at a lower risk of health conditions than an older person. Since the risk to your life or health is low, the term plan premiums will also be low. As you age, you are at a greater risk of developing lifestyle diseases and other health conditions which need proportionate life insurance coverage. Hence, the premiums will also be higher.

9. Will my occupation impact my term insurance premium?

If you have a risky occupation or a job where your life or your health may be at risk, your term plan premiums will be high. The greater the risk, the higher the premium. For instance, a person who is in the mining business will have a higher term plan premium as compared to a teacher or professor.

10.Which factors determine the term insurance premium?

Your term insurance premium will be determined as per your age, your term policy sum assured, the premium paying term, and the policy term. There are also other factors, such as your health condition, your family’s medical history, your occupation, and lifestyle habits, that will be considered while deciding your term insurance premium.

If you want to find out how to calculate your term plan premium, you can simply use a term insurance calculator that will help you know your premium instantly based on these factors.

11. What is the impact on term policy premiums for smokers?

If you are a smoker and want to purchase a term insurance plan, your premiums will be calculated as per your sum assured. You can use a term plan calculator to know your premium amount. However, you will not be able to avail of any special premium rates that are offered to women policyholders and non-smokers.

1.How many times can one file a term insurance claim?

A term insurance claim can only be filed once in case the policyholder meets their untimely demise during the policy tenure. Once the death benefit is paid out to the nominee, the coverage ends, and no other benefits can be offered on the policy.

2.How do I file a term insurance claim?

To file a term insurance claim, contact us through any of the following channels:

- Email : customercare@tataaia.com

- Call - 1860-266-9966 (local charges apply)

- Visit us at any Tata AIA Life Insurance Company branch office.

- Write to us at :

The Claims Department,

Tata AIA Life Insurance Company Limited

B- Wing, 9th Floor,

I-Think Techno Campus,

Behind TCS, Pokhran Road No.2,

Close to Eastern Express Highway,

Thane (West) 400 607.

IRDA Regn. No. 110

3.What are the different term insurance claims that can be filed?

You can file a death claim on a term insurance policy. In case you have added a critical illness cover to your plan, you can also file a claim for the same if you are diagnosed with a critical illness.

4.How to ensure that my family receives a timely death benefit?

To ensure that your family does not face any hassles at the time of claim settlement, choose a reputed insurance provider with a high claim settlement ratio and fill up your insurance proposal form with correct and accurate details.

Tata AIA Life Insurance has an individual death claim settlement ratio of 99.13% for FY 2022-23$

5.What if my nominees want to file a claim in India from another country?

If your nominee wants to file the claim from outside India, they can upload the attested copies of the essential documents online and send them to us by email. To file a claim offline, they can courier these documents to their representative in India, who can submit them to us at any of our offices.

6.Are COVID-19 claims covered under the Tata AIA term policy?

Yes, all Tata AIA term insurance policies are designed to cover COVID-19-related death claims.

7.Can a claim be rejected?

A claim can be rejected due to different reasons. These are some of the common reasons for claim rejection:

- False information in the policy proposal form.

- Withholding crucial health-related information during policy purchase.

- Wrong or incorrect nominee details/information.

8.Will the claim be settled if I die within one year of the policy purchase?

Tata AIA settles claims for all deaths, subject to the completion of some premium payments. In the case of death by suicide within the first policy year, the claim will be settled as per specific policy terms.

- Tata AIA Sampoorna Raksha Promise - Non-Linked, Non-Participating, pure risk, Individual Life Insurance Product (UIN:110N176V05)

- Tata AIA Maha Raksha Supreme Select - Non-Linked, Non-Participating, Pure Risk, Individual Life Insurance Product (UIN: 110N171V08)

- 1With this feature, instant death benefit of INR 3 Lacs from the Sum Assured will be paid within 1 working day from the claim registration date. This feature is applicable only after a waiting period of 3 policy years from the policy inception or revival of the policy and provided the policy is in force. The remaining SA shall be payable post the completion of the claim investigation. Further, in case of any discrepancy in the claim investigation resulting in the final decision of non-payment of the claim, the company reserves the right to recover the already paid amount. The acceleration of instant claim should not be construed/interpreted as acceptance of the claim.

- 2Individual Death Claim Settlement Ratio is 99.13% for FY 2023 - 24 as per the latest annual audited figures.

- 3Income Tax benefits would be available as per the prevailing income tax laws, subject to fulfillment of conditions stipulated therein. Income Tax laws are subject to change from time to time. Tata AIA Life Insurance Company Ltd. does not assume responsibility on tax implication mentioned anywhere in this document. Please consult your own tax consultant to know the tax benefits available to you.

- 4Rider is not mandatory and is available for a nominal extra cost. For more details on benefits, premiums, and exclusions under the Rider, please contact Tata AIA Life's Insurance Advisor/ branch.

- 585,76,889 families protected till 31st December 2024.

- 6Applicable to only non-early claims with more than 3 years of policy duration, non-investigation cases, up to Sum Assured of Rs. 50 lakhs. Applicable for branch walk in. Time limit to submit claim to Tata AIA Life Insurance is 2 pm on working days. Subject to submission of complete documents. Not applicable for ULIP policies and open title claims.

- 7With FlexiPay Benefit, policyholder is allowed to defer the due premium for a period of 12 months while maintaining the full risk cover under the base plan and attached riders. At the end of Premium Deferment period, the policyholder is required to pay the due premiums, including the premium applicable for the period of Premium Deferment, i.e. the base cover premium and additional premium (if any). | This benefit shall be available for multiple times with a gap of 5 policy years from the expiry date of previous Premium Deferment. The option can be exercised only after payment of 5 full years premium. | No interest shall be levied on the premium due during the Premium Deferment period. If the premiums due are not paid within the grace period after expiry of the Premium Deferment, the Policy (including Rider(s), if any) shall lapse and no benefits shall be payable in the Policy or the Rider(s), if any) and company shall be entitled to recover the same from any amounts or This benefit payable under the Policy or Rider(s).

- 8Tata AIA Sampoorna Raksha Promise offers first year digital discount of 1% for Single Pay, 10% for Limited Pay/Regular Pay. This product offers first year premium discount of 8.5% for Limited Pay/Regular Pay and 1% for Single Pay to salaried customers.

- 9Tax benefits of up to ₹46,800 u/s 80C is calculated at highest tax slab rate of 31.20% (including cess excluding surcharge) on life insurance premium paid of ₹1,50,000 as per old tax regime. Tax benefits under the policy are subject to conditions laid under Section 80C, 80D,10(10D), 115BAC and other applicable provisions of the Income Tax Act,1961. Good and Service tax and Cess, if any will be charged extra as per prevailing rates. The Tax Free income is subject to conditions specified under section 10(10D) and other applicable provisions of the Income Tax Act,1961. Tax laws are subject to amendments made thereto from time to time. Please consult your tax advisor for details, before acting on above.

- 10Not applicable under PoS, please refer sales brochure for more information

- 11As on 3rd April 2024, the company has a total Assets Under Management (AUM) of ₹1,00,099.11 Crore

- 12Tata AIA Maha Raksha Supreme Select offers Premium discount of 1% of single premium and 8.5% on first year premiums for regular and limited pay to the salaried customers.

- ^Under Life Promise Plus Option, an amount equal to the 100% of the Total Premiums Paid (excluding loading for modal premiums) shall be payable at the end of the Policy Term, provided the life assured survives till maturity and the policy is not terminated earlier.

- #Retail Sum Assured for FY2023 is Rs 4,43,479 Crores

- $$Illustrated Premium is the monthly premium excluding taxes for 20 yr. old female, Standard Life, Non-Smoker for ₹ 1 Cr. Sum Assured with Policy Term of 20 yrs. (Regular Pay) under Life Promise Option with first year premium discount for digital purchase and salaried person. Please refer Benefit Illustration for more details. Premium is subject to applicable taxes, cesses & levies which will be entirely borne/ paid by the Policyholder, in addition to the payment of such Premium. Tata AIA Life shall have the right to claim, deduct, adjust, recover the amount of any applicable tax or imposition, levied by any statutory or administrative body, from the benefits payable under the Policy. Kindly refer the sales illustration for the exact premium.

- ##Illustrated Premium is the monthly premium excluding taxes for 20 yr. old female, Standard Life, Non-Smoker for 2 Cr. Sum Assured with Policy Term of 20 yrs. (Regular Pay) with Life Secure plan option with first year premium discount for digital purchase and salaried person. Please refer Benefit Illustration for more details. Tata AIA Life shall have the right to claim, deduct, adjust, recover the amount of any applicable tax or imposition, levied by any statutory or administrative body, from the benefits payable under the Policy. Kindly refer the sales illustration for the exact premium.

- This product is underwritten by Tata AIA Life Insurance Company Ltd.

- Insurance cover is available under this product.

- In case of non-standard lives, extra premiums will be charged as per our underwriting guidelines.

- For more details on risk factors, terms and conditions please read sales brochure carefully before concluding a sale.

- This plan is not a guaranteed issuance plan, and it will be subject to Company’s underwriting and acceptance.

- Premium will vary depending on the option chosen

- Buying a Life Insurance Policy is a long-term commitment. An early termination of the Policy usually involves high costs, and the Surrender Value payable may be less than the all the Premiums Paid.

- In case of POS variant, the product is available with/without medical underwriting as per BAUP (Board Approved Underwriting Policy)

- L&C/Advt/2025/Mar/1455