Discounted HPV vaccinations1 for cervical cancer prevention

Discounted HPV vaccinations1 for cervical cancer prevention

Call us

Call us

FOR EXISTING POLICY

FOR EXISTING POLICY

Have query on premium, payout or any servicing need?

Call us:

FOR NEW POLICY

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY (NRIs)

Note: Consent is provided to Tata AIA Life Insurance Company Limited to contact you by calling/giving missed call to the above numbers.

Thank you for sharing your details. To receive a call from Tata AIA Financial Advisor.

reCAPTCHA is not working.

No relevant search results found.

Discounted HPV vaccinations1 for cervical cancer prevention

Up to 18.5% discount2 on first-year premium

Waiver of Premium on Husbands’s accidental death3

Life cover + Wealth creation option

T&C apply

Need assistance in choosing a new plan?

Kindly enter the OTP sent to

Please enter valid OTP

01:60

Didn't receive OTP?

Your details have been successfully submitted. A representative from Tata AIA Life Insurance will call you soon.

Your details could not be saved.

Please try again.

Your premium calculation is in progress

Life insurance for women is a financial cover designed to protect a woman’s income, responsibilities, and future plans. It is important today because women are managing careers, families, and long-term goals at the same time. A reliable policy helps create a strong safety net so that, in many cases, financial stability continues even when life takes an unexpected turn.

Protect the financial future of your loved ones against uncertainties of life with our Term Insurance plans that offers you larger cover, higher security, and speedy settlement.

Non-Linked, Non-Participating, Pure Risk, Individual Life Insurance Product (UIN:110N176V12)

Non-Linked, Non-Participating, pure risk, Individual Life Insurance Product (UIN:110N176V12)

Discover Complete Health and Wealth: Our comprehensive plan is designed to take care of your health, wellness, and financial security—all in one, just for you.

In This Policy, The Investment Risk in Investment Portfolio Is Borne by The Policyholder

Grow your wealth with our guaranteed return plans for a fikar-free future and save on tax6.

Individual, non-linked, participating, Life Insurance Savings Plan (UIN: 110N207V02)

Non-Linked, Non-Participating, Individual Life Insurance Savings Plan (UIN: 110N158V14)

Plan your retirement wisely with a suitable pension plan for peace of mind in your golden years

A Non-Participating, Unit Linked, Individual Life Insurance Pension Plan (UIN: 110L182V09)

A Non-Linked, Non-Participating, Annuity Plan (UIN:110N161V13)

Life insurance for women is a plan that offers financial protection along with the option to build savings over time. You pay regular premiums, and in return, the policy provides a payout to your nominee if something happens to you. Many times, it also helps you create a disciplined savings habit.

What makes it useful is its flexibility. It can grow with your needs. Whether you are working, taking a career break, or planning for retirement, a life insurance plan can be adjusted to match your situation. In practice, across the industry, these plans are used by many women as a complete solution that combines protection and financial planning. It is one of those tools that makes a real difference when used with a clear plan.

In case of any unfortunate event, your life insurance plan will pay out a death benefit to your family that will help them sustain their livelihood. This ensures that all their dreams are fulfilled even when you are not around.

A life insurance policy helps you save money for your future goals. That way, you need not depend on loans and credit for funding your future financial commitments, such as caring for your parents and children or starting a new venture.

In case you have unpaid loans and debts, in your absence, the burden of repaying these debts should not fall on your loved ones. The policy cover can protect their life savings by taking care of these loans and debts.

As a woman, planning your own retirement gives you greater financial independence to acknowledge your needs at the later years of your life. With adequate financial resources during retirement, you can support your wellbeing and be a support to your family.

In times of medical emergencies, your life insurance can protect you and your family against critical illnesses, accidental death, disability, etc., if you add the necessary optional riders10 to your insurance plan.

You can get income tax6 benefits on the premium amount paid and maturity benefits received on your life insurance policy.

Different plans are available, and each works for different needs. Let’s look at the main options.

The need for life insurance has grown over the past few years. As roles change, financial planning becomes more important. Here’s why it matters.

Your Insurance Needs

Life Stage Needs

Policy Term

Claim Settlement Ratio

A life insurance policy is important for everyone, especially for women, since they also take up a major chunk of their personal and financial responsibilities. By purchasing a life insurance policy, a woman can protect her family from financial insecurities that may arise due to her death or an accidental disability.

A woman can determine her policy's necessary life insurance coverage based on her needs. Calculating the Human Life Value (HLV) is another way of calculating life insurance coverage, wherein one can compute the current value of profits, expenses, debts, and savings. This method can help you determine the amount needed to secure your family’s needs in your absence.

You can also use any of our Tata AIA Life Insurance calculators to get a fair idea of the premium you need to pay for a desired amount of coverage and adjust the variables accordingly.

Since housewives take on a lot of household responsibilities that cannot be computed on a monetary basis, a life insurance plan, such as a term plan, is a must for her. This is because the whole family depends on her to manage the house and the family and plan the finances.

In her absence, finding help to fulfil these responsibilities requires extensive financial assistance. Hence, homemakers must have a term insurance policy.

No, life insurance for women can be quite affordable as Tata AIA Life Insurance offers preferential premium rates for women policyholders.

Yes, a homemaker can opt for a life insurance plan, such as a term plan that offers extensive life insurance coverage or a savings plan that can help one save a financial corpus for the future.

The policy term for your life insurance policy can be as flexible as you want it to be. Since some Tata AIA Life Insurance plans offer whole life coverage of up to 100 years, you can opt for the same and enjoy uninterrupted coverage for your entire lifetime without the hassle of renewals and new policy purchases.

Women can claim tax6 deductions on their policy premiums under Section 80C of the Income Tax Act, while the death benefit paid out on the policyholder’s demise is tax-exempt under Section 10(10D) of the Income Tax Act.

The maturity benefits on a savings plan, and Unit-Linked Insurance Plan are also eligible for the Section 10(10D) exemption, subject to certain policy terms and conditions.

Tata AIA Life Insurance offers lower premium rates to women policyholders. However, you can also save money on your life insurance premiums by using our Tata AIA Life Insurance premium calculator, which helps you choose adequate coverage and pay reasonable premiums.

While having a joint life insurance policy with one’s spouse is suitable, women should also have a separate life insurance plan that is customized to suit their individual needs and where they are the primary policyholder.

For instance, they can select a sum assured and a policy term of their life insurance plan based on their financial goals that will be different from the coverage and policy tenure of the joint life insurance policy.

Yes, life insurance is accessible to and necessary for self-employed women who want to secure their families from unforeseen financial risks such as debts, other liabilities, and financial emergencies in their absence.

Women with pre-existing health conditions can avail of life insurance policies. However, as per the policy guidelines, there may be a waiting period for the pre-existing disease, after which the policy coverage and benefits will be active.

It is also necessary to select a life insurance policy that offers coverage for your pre-existing health condition and related conditions to secure yourself and your family against financial uncertainties.

Women can pick the right life insurance policy based on their own and their family’s financial needs. For instance, if one only needs pure and extensive life cover for their family’s financial security, a term plan with adequate coverage can be a suitable choice. However, if the woman wants to plan her future savings in advance, a savings plan such as an endowment or money-back policy can be a good option.

The best age for women to get life insurance is in their 20s or 30s, as premiums are lower, however, it's never too late to consider life insurance based on individual needs.

Popular Searches

Disclaimer

The linked insurance product do not offer any liquidity during the first five years of the contract. The policy holder will not be able to surrender/withdraw the monies invested in linked insurance products completely or partially till the end of the fifth year.

Shubh Shakti is a combination of Tata AIA Sampoorna Raksha Promise (Non-Linked, Non-Participating, Pure Risk, Individual Life Insurance Product) UIN:110N176V12 and Tata AIA Health Buddy (Non-Participating, Non-Linked Individual Health Product) UIN: 110N183V01. Tata AIA Sampoorna Raksha Promise are also available for sale individually without the combination offered/ suggested.

Tata AIA Shubh Flexi Income Plan (UIN: 110N207V02) - Individual, Non-Linked, participating, Life Insurance Savings Plan

The complete name of Tata AIA Fortune Guarantee Plus is Tata AIA Life Insurance Fortune Guarantee Plus - Non-Linked, Non-Participating, Individual Life Insurance Savings Plan (UIN: 110N158V14).

Param Raksha Life Pro+ is designed for combination of benefits of following individual and separate products named (1) Tata AIA Smart Sampoorna Raksha Supreme Unit Linked, Non-Participating Individual Life Insurance Plan (UIN: 110L179V02) and (2) Tata AIA Vitality Protect Advance - A Non-Linked, Non- Participating Individual Health Product (UIN: 110N178V01).

The complete name of Tata AIA Fortune Guarantee Pension is Tata AIA Life Insurance Fortune Guarantee Pension (UIN:110N161V13) - A Non-Linked Non-Participating Individual Life Insurance Plan.

Tata AIA Smart Pension Secure (UIN: 110L182V09) - Non-Participating, Unit Linked, Individual Life Insurance Pension Plan

Tata AIA Premier SIP is a combination of the Tata AIA Smart SIP, a non-participating, unit-linked, individual life insurance savings plan (UIN: 110L174V02), and Tata AIA Health Buddy, Non-participating, Non-Linked, Individual Health Product (UIN:110N183V01). Both Tata AIA Smart SIP and Tata AIA Health Buddy are also available for sale individually

These products are also available for sale individually without the combination offered/ suggested. This benefit illustration is the arithmetic combination and chronological listing of combined benefits of individual products. The customer is advised to refer to the detailed sales brochure of respective individual products mentioned herein before concluding sale.

1Vaccination at discounted price is available under HB Enhance. Discount is through way of wallet i.e. wallet for vaccinations. (Rs 500 per prescribed vaccination 4 transactions allowed = Rs 2,000).

2As per the duly approved product design and terms & conditions of the product, this includes first year digital discount of 10% for Limited Pay/Regular Pay and 8.5% salaried discount. For Single Pay, 1% discount will be available for online purchase and salaried discount each.

3Under waiver of premium on husbands’ accidental death, all future premiums payable by the Life Assured shall be waived off and the policy shall continue to stay in force till the end of the Policy Term. Please refer to the full policy document for more details

4As per the duly approved product design and terms & conditions of the product, Illustrated premium of ₹501 is the monthly premium for a 20 yr. old female, Standard Life, Non-Smoker for ₹1 Cr. Sum Assured with Policy Term of 20 yrs. (Regular Pay) under Life Promise Option of Tata AIA Sampoorna Raksha Promise with first year premium discount of 10% for digital purchase and 8.5% for salaried person. Please refer Benefit Illustration for more details.

5Under Life Promise Plus Option, an amount equal to 100% of the Total Premiums Paid (excluding loading for modal premiums) shall be payable at the end of the Policy Term, provided the life assured survives till maturity and the policy is not terminated earlier.

6Income Tax benefits would be available as per the prevailing income tax laws, subject to fulfillment of conditions stipulated therein. Income Tax laws are subject to change from time to time. Tata AIA Life Insurance Company Ltd. does not assume responsibility on tax implication mentioned anywhere in this document. Please consult your own tax consultant to know the tax benefits available to you.

No Goods and Service Tax shall be applicable on Individual life insurance products as per prevailing laws. Tax laws are subject to amendments from time to time. If any imposition (tax or otherwise) is levied by any statutory or administrative body under the Policy, Tata AIA Life Insurance Company Limited reserves the right to claim the same from the Policyholder.

9Return of Premium shall be the sum of Guaranteed Maturity Benefit plus Milestone Benefit and shall be payable at the end of the Income Period, irrespective of survival of the life insured(s) during the Income Period.

10Rider is not mandatory and is available for a nominal extra cost. For more details on benefits, premiums, and exclusions under the Rider, please contact Tata AIA Life's Insurance Advisor/ branch

12All funds open for new business which have completed 5 years since inception are rated 4 star or 5 star by Morningstar as of August 2025.

©2025 Morningstar. All rights reserved. The Morningstar name is a registered trademark of Morningstar, Inc. in India and other jurisdictions. The information contained here: (1) includes the proprietary information of Morningstar, Inc. and its affiliates, including, without limitation, Morningstar India Private Limited (“Morningstar”); (2) may not be copied, redistributed or used, by any means, in whole or in part, without the prior, written consent of Morningstar; (3) is not warranted to be complete, accurate or timely; and (4) may be drawn from data published on various dates and procured from various sources and (5) shall not be construed as an offer to buy or sell any security or other investment vehicle. Neither Morningstar, Inc. nor any of its affiliates (including, without limitation, Morningstar) nor any of their officers, directors, employees, associates or agents shall be responsible or liable for any trading decisions, damages or other losses resulting directly or indirectly from the information.

13The Insured Amount under this option is payable on earlier of death or diagnosis of Terminal illness of the Life Insured. Please refer Terms and Condition for more details.

14Partial withdrawals only available 3 times during the entire policy term and only for reasons specified in IRDA Regulations as amended from time to time

15The word Guaranteed and Guarantee means the annuity payout is fixed at inception of the policy and will be payable for whole of life or till death of the Annuitant(s)

1698,01,699 families protected till 18th May 2026.

17Retail Sum Assured for FY 2025-26 is ₹9,00,876 Crore. https://irdai.gov.in/document-detail?documentId=6552249

18As on 31st March 2026, the company has a total Assets Under Management (AUM) of ₹145,589 Crore

19Individual Death Claim Settlement Ratio is 99.45% for FY 2025-26

20Applicable to only non-early claims more than 3 years of policy duration, non-investigation cases, up to Sum assured of 50 lacs. Applicable for branch walk in. Time limit to submit claim to Tata AIA by 2 pm (working days). Subject to submission of complete documents. Not applicable to ULIP policies and open title claims.

22Premium break due to pregnancy is an inbuilt feature that is allowed twice during the premium paying term, subject to a two-year gap and prior intimation 60 days in advance. This feature activates only after payment of two full years’ premiums. Please refer to the full policy document for more details

23Cash bonuses (if declared) may be opted to be paid out at the end of the chosen pay-out frequency or as premiums offset. Alternatively, the cash bonus (if declared) can be chosen to be accumulated and paid out on maturity, death or surrender. Cash bonuses are applicable for Early income and Deferred income option. Please refer Brochure for additional details.

24Cash bonuses, if declared, may be fully or partially received in the sub-wallet. The policyholder may withdraw the sub-wallet balance, in part or in full, at any time during the policy term. The current loyalty addition rate on the Sub-wallet will be 5.25% compounding monthly. The loyalty addition rate shall be at which RBI absorbs liquidity which is the reference rate from Standing Deposit Facility rate. The current Standing Deposit Facility rate is 5.25% p.a. and the same shall be reviewed bi-monthly.

For ULIP products

The fund is managed by Tata AIA Life Insurance Company Ltd. For more details on risk factors, terms and conditions please read Sales Brochure carefully before concluding a sale. The precise terms and conditions of this plan are specified in the Policy Contract.

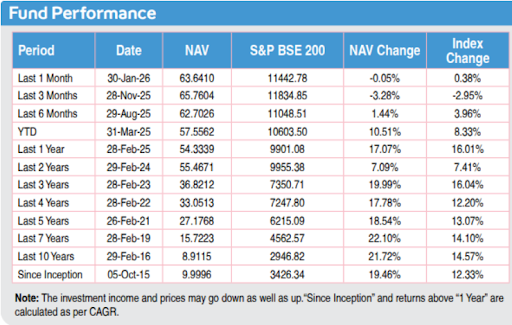

Past performance is not indicative of future performance. Returns are calculated on an absolute basis for a period of less than (or equal to) a year, with reinvestment of dividends (if any).

Investments are subject to market risks. The Company does not guarantee any assured returns. The investment income and price may go down as well as up depending on several factors influencing the market.

Risk cover commences along with policy commencement for all lives, including minor lives. Buying a Life Insurance Policy is a long-term commitment. An early termination of the Policy usually involves high costs, and the Surrender Value payable may be less than the all the Premiums Paid. In case of non-standard lives and on submission of non-standard age proof, extra premiums will be charged as per our underwriting guidelines. All Premiums and interest payable under the policy are exclusive of applicable taxes, duties, surcharge, cesses, or levies which will be entirely borne/ paid by the Policyholder, in addition to the payment of such Premium or interest. Tata AIA Life shall have the right to claim, deduct, adjust, and recover the amount of any applicable tax or imposition, levied by any statutory or administrative body, from the benefits payable under the Policy.

The risk factors of the bonuses projected under the product are not guaranteed.

Past performance doesn't construe any indication of future bonuses.

These products are subject to the overall performance of the insurer in terms of investments, management of expenses, mortality and lapses.

For more details on risk factors, terms and conditions please read sales brochure carefully before concluding a sale.

Please make your own independent decision after consulting your financial or other professional advisor.

The fund is managed by Tata AIA Life Insurance Company Ltd. (hereinafter the “Company”).Tata AIA Life Insurance Company Limited is only the name of the Insurance Company & Tata AIA Smart SIP, Tata AIA Sampoorna Raksha Supreme, Tata AIA Smart Pension Secure, is only the name of the Unit Linked Life Insurance contract and does not in any way indicate the quality of the contract, its future prospects or returns.

Unit Linked Life Insurance products are different from the traditional insurance products and are subject to the risk factors. Please know the associated risks and the applicable charges, from your Insurance Agent or Intermediary or Policy Document issued by the Insurance Company.

Various funds offered under this contract are the names of the funds and do not in any way indicate the quality of these plans, their future prospects and returns. The underlying Fund's NAV will be affected by interest rates and the performance of the underlying stocks.

The performance of the managed portfolios and funds is not guaranteed, and the value may increase or decrease in accordance with the future experience of the managed portfolios and funds.

The premium paid in Unit Linked Life Insurance policies are subject to investment risks associated with capital markets and the NAVs of the units may go up or down based on the performance of fund and factors influencing the capital market and the insured is responsible for his/her decisions. The various funds offered under this contract are the names of the funds and do not in any way indicate the quality of these plans, their future prospects and returns. On survival to the end of the policy term, the Total Fund Value including Top-Up Premium Fund Value valued at applicable NAV on the date of Maturity will be paid

The investment income and price may go down as well as up depending on several factors influencing the market. Please know the associated risks and the applicable charges, from your Insurance Agent or the Intermediary or Policy Document issued by the Insurance Company. Please make your own independent decision after consulting your financial or other professional advisor. Returns are calculated on an absolute basis for a period of less than (or equal to) a year, with reinvestment of dividends (if any). All investments made by the Company are subject to market risks. The Company does not guarantee any assured returns.

The performance of the managed portfolios and funds is not guaranteed, and the value may increase or decrease in accordance with the future experience of the managed portfolios and funds. The solutions are underwritten by Tata AIA Life Insurance Company Limited

This product is underwritten by Tata AIA Life Insurance Company Ltd.

The plan is not a guaranteed issuance plan, and it will be subject to company’s underwriting and acceptance.

Life insurance cover is available under the solution. For details on products, associated risk factors, terms and conditions please read Sales Brochure carefully before concluding a sale.

Buying a Life Insurance Policy is a long-term commitment. An early termination of the Policy usually involves high costs, and the Surrender Value payable may be less than the all the Premiums Paid.

In case of non-standard lives and on submission of non-standard age proof, extra premiums will be charged as per our underwriting guidelines.

L&C/Advt/2026/Jun/3941

Reviewed by

Reviewed by

.svg)